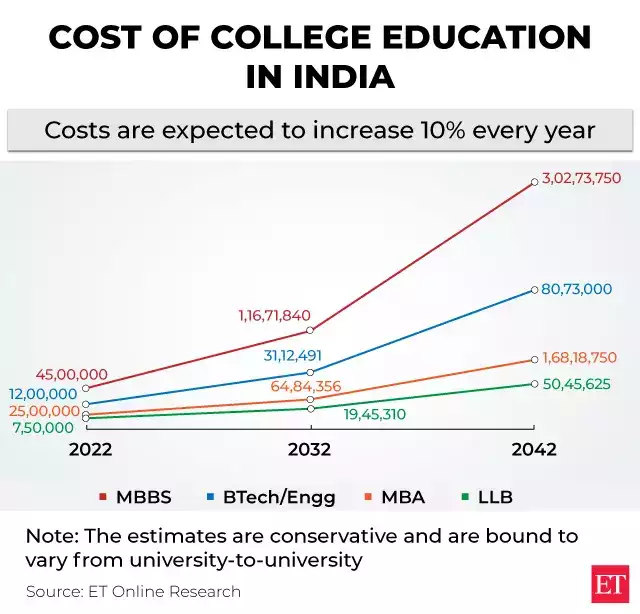

Did you know that over 70 % of Indians are worried about funding their child’s education and are seeking child investment plans? These costs are rising by 10-12% per year and, therefore, planning for your child’s future should be a high priority. Some new estimations indicates that due to inflation and hike in the tuition fees the cost of attaining higher education in India could cross ₹50 lakhs in 2030. With regard to this, it implies that unless early investment is made in education funding these costs are inevitable.

To manage this cost burden, parents need to invest in other forms of investment products that are safe, have higher returns and most importantly have a tax advantage. This blog details the 6 best child investment plans for 2024 to ensure your child has a financially secure future while also growing your wealth as a parent.

Why Invest in Child Investment Plans?

Child investment plans are one of the best schemes to secure the future of your child as well as to ensure you are financially secure to incur major expenses of life like education and marriage. portraits a right combination of high return and safe rate investments hence no frequent withdrawal from the retirement account to fund your child’s dreams. Whereas tuition fees remain high, inflation corrodes the savings, it is time to start planning ahead. Whether you invest in a PPF, an SSY, mutual funds, or another investment plan, the most essential thing is to start early and consistently.

Here are 6 Best Child Investment Plans For safeguarding their Future

1. Public Provident Fund (PPF) for Long-Term Stability

PPF is one of the most reliable options when it comes to investment in the future of the child among Indian parents. It has a comparatively small, fixed interest rate of 7.1% per year compounded yearly (as of 2024). This is because the PPF has a lock-in period of 15 years. The kind of financial goals that can be financed from the policy by their maturity period include your child’s higher education or marriage. PPF as a Child Investment Plan is another savvy investment scheme in India because the amount that investors contribute to the PPF is exempt from tax under Section 80C while the maturity amount of the scheme is legally tax-free. For instance, you provide ₹100,000 each year towards a PPF account for the child till he/she turns college going age, you will have over ₹30 lakh.

2. Sukanya Samriddhi Yojana (SSY) for Daughters

For those who have a daughter then Sukanya Samriddhi Yojana (SSY) is the best Child investment plan. SSY provides the highest interest rate among the squirting amines schemes which are the small saving schemes at 8% making it the best scheme for parents to secure their daughter’s future. This scheme is introduced by the government where the parents can invest up to the age of 21 years of the daughter’s age so you can fund all her important stages in life including her education and marriage. Also, investments of up to ₹1.5 lakh per financial year are allowed as a deduction from gross total income under Section 80C of the Income Tax Act and the interest earned is also tax exempt. From the case of SSY, high return, and tax-free status make SSY a good investment plan for your daughters financial security in the future.

3. Equity Mutual Funds

Equity mutual funds as child investment plans are especially suitable for parents willing to undertake higher risks of their investment with a view to having comparatively better returns. On a long run scenario basis, equity mutual funds themselves have delivered returns of between 12-15% per annum in the past and are much higher even than PPF or FDs currently. Just imagine investing a small amount of your earnings through Systematic Investment Plan (SIP) mode in child-specific equity mutual fund for many years and that’ll give a huge amount someday. For instance, if you invest ₹10,000 per month in a mutual fund with a 12% expected return, you could reach up to ₹50 lakh in 15 years. This money can be used for your child’s higher education whether locally or internationally.

4. Unit Linked Insurance Plans (ULIPs) for Dual Benefits

Unit Linked Insurance Plan as child investment plans for dual benefits offers insurance facility along with investment. This feature of mutual functioning has a double advantage, which makes it appropriate for parents who would like to financially secure a child, as well as to increase their own capital continuously. Using ULIPs you can invest in both equity and debt depending on your risk taking capacity and the risk that you want to take. But in the long run, they more or less can give a return of anything between 8-10 percent, which makes them a good investment for creating wealth. ULIPs also enjoy tax benefits that come with sections 80C and 10(10D) allowing you to reduce your tax burden as you invest for your child’s future. Since one has the option of moving from one fund to another, they are perfect for creating a corpus for ones child’s education or any other need.

5. Child Education Funds for Goal-Oriented Savings

Child education funds are financial solutions created to enable the parent to save money towards his child’s education. These plans also offer propositions like Insurance + Investment for your child’s future education is not in any way affected by your demise. They also provide fixed maturity benefits on milestones in your child’s education process, for instance, college or postgraduate. Many child education plans as mentioned earlier are very flexible, and their premiums are charged to cater for the increased cost of educating the child. Also, these plans have the element of maturity benefit and it tends to help in payment for a child’s education or some other large expenses.

6. Fixed Deposits (FDs) for Guaranteed Returns

For parents who love to take a conservative approach for their money investments, fixed deposits or FDs still hold good. Interest rate has ranged from 6-7 % in 2024 and though it is lower compared to other investment opportunity, FD is safe investment with assured returns more suitable for the risk adverse investors. FDs can be taken for any number of years which can possibly have maturity date when your child may require it especially for higher education. You can also select child rated FDs that makes provisions for auto renewal of the account and besides it allows partial withdrawals to sponsor education. While FDs are not as tax friendly as PPF or SSY they are secure and will provide a regular income which is good for parents.

Conclusion

As costs of education and financial insecurity keeps increasing, investing in child investment plans becomes an important priority. The predictable returns on offer with PPF and FDs or the higher returns possible with mutual funds and ULIPs, it has a child investment plan for everyone. It’s important not to delay all your investments. And so, if you choose mutual funds, you can use Edufund’s College Cost Calculator to calculate your investment goals in just 2 minutes.