Systematic investment plans, or SIP, are a great tool to invest. It has helped create a significant amount of wealth over time for many investors. Some basic investment plans have the potential to create substantial wealth over time. Three basic principles work in favour of a SIP –

- The earlier you start investing, the more the return accumulates over time. This leads to more profits. This phenomenon is also known as the power of compounding in financial parlance.

- Time plays a more crucial role in SIP than timing. The earlier you start, the more you make; the longer you remain invested, the more you gain. This phenomenon also supports why a regular SIP has a better wealth ratio than a step-up SIP. For our novice readers, step-up SIP is where you tend to increase the amount of SIP every year when your inflows increase.

- An investor needs to remember two things to get the power of compounding. Firstly, leveraging the power of equities helps in the long run, and secondly, the accumulated profits should remain reinvested to reap further benefits.

Can a small SIP of Rs 5,000 make a big difference?

Yes, very much! Even a tiny amount can make a huge difference. How much difference can a SIP of Rs 5,000 per month make to your wealth?

The answer is that it can make a big difference if you continue the investment for the long term in a disciplined manner without withdrawing any investments and investing in a powerful asset class such as equities.

Now, the question is, how much wealth can be accumulated?

For the answer, consider the chart below.

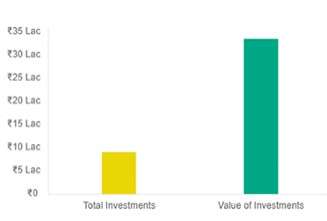

How the monthly SIP of Rs 5K grow over 15 years

As seen from the above chart, a SIP of Rs 5,000 can grow your wealth to Rs 33.43 Lakh in 15 years. We have considered the annual return to be around 15%.

15% may look on the higher side, but remember, when you have a long-term horizon, such as 15 years, you can avoid the conservative plan altogether.

If you have a conservative approach with a long-term horizon, it is nothing but not utilizing the true potential of capital. Your risk appetite and investment horizon should trickle down to your expected returns.

Also, risk appetite should be computed by taking into account the cash inflow, minimum essential expenditure, age, number of dependents, and the like.

How to choose the SIP instruments?

Once you have understood your risk appetite and investment horizon, you need to map the same with the funds. Equity funds are best suited for a horizon over five years, particularly the ones that invest in mid and small-cap names.

Team EduFund has mapped the ideal time horizon and risk levels for the different fund categories (refer to the table below).

| <1 year | 1 – 3 years | 3 – 5 years | >5 years | |

| Low risk | Debt: Liquid Debt: Ultra-short term | Debt: Short term | Debt: Long term | Hybrid: Balanced |

| Medium risk | Debt: Short term | Debt: Long Term Hybrid: Balanced | Hybrid: Balanced Equity: Large-cap Equity: Multicap | Equity: Large-cap Equity: Multicap |

| High risk | Debt: Long term Equity: Sector | Equity: Large cap Equity: Sector | Equity: Midcap Equity: Sector | Equity: Midcap Equity: Smallcap |

Considering the same, let us see the corpus you may make when your risk appetite differs.

| Risk Appetite | Investment category | Expected returns | Invested amount | Expected amount |

| Low risk | Hybrid: Balanced | 10% | 9 Lakhs | 20.72 Lakhs |

| Medium risk | Equity: Midcap | 12% | 9 Lakhs | 23.98 Lakhs |

| High risk | Equity: Small Cap | 15% | 9 Lakhs | 33.43 Lakhs |

As seen in the table above, the returns are highest in the high-risk category, and even a small amount of Rs 5000 per month for 15 years could help you fetch nearly 4x wealth in 15 years.

Should you invest Rs 5000 in one fund?

The answer is No. If you do that, you will get into concentration risk where your capital will be invested only in one fund. Remember, you need to have a diversified portfolio to benefit from each of them and, at the same time, reduce the volatility at the portfolio level by having smaller portions in each.

You should select 1-3 funds to make it Rs 5000 per month.

At this juncture, let us introduce a very cool feature of your app EduFund – the Educases. The Educases in EduFund are devised to ensure you invest systematically over the very long-term/long-term/short-term/very short-term for higher education goals, short-term goals, etc.

Besides, the investment strategies section also highlights the five risk profiles and accordingly recommends the funds for investment. The tool uses its proprietary AI-backed engine that goes through multiple permutations and combinations before throwing any funds that suit the investor best.

Not to mention that every result is back-tested to ensure that the EduFund-recommended funds do a great job in outperforming the benchmark and inflation by considerable margins.

The following are some of the funds recommended by EduFund that an investor could look at if they are willing to invest in the long-term and have a high investment horizon of 15 years and a high-risk appetite.

The above-mentioned Rs 5000 SIP could be invested in the following funds to achieve 4x growth.

| Fund Name | Amount | Objective |

| Canara Robeco Small Cap Fund | 2500 | The fund seeks to provide long-term capital appreciation by investing predominantly in small companies |

| PGIM India Midcap Opportunities Fund | 2500 | The fund seeks to achieve long-term capital appreciation by investing primarily in equity and equity related instruments |