Does time in the market beat timing the market?

What is market timing? Does time in the market beat timing the market? Everyone wants to maximize their portfolio returns by timing the market. This is why you’ve probably wondered what is the best date you can choose for your SIPs in Mutual Funds.

But does timing your SIP dates help, in the real world? Let’s find out in this short article.

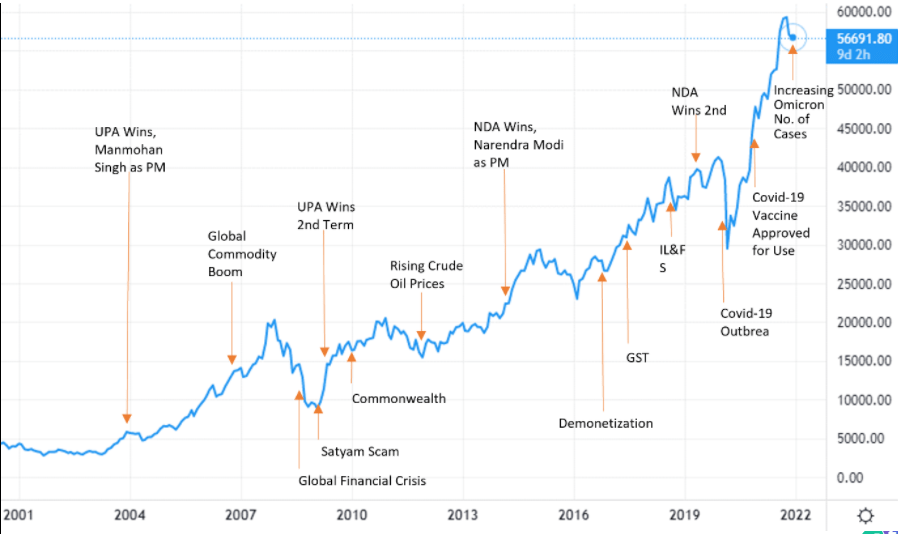

Look at the picture below. The market will always have short-term fluctuations/downfalls. However, if you look at the big picture or the overall trend of the market, you will realize that it is always positive/rising.

Staying invested for a longer period irrespective of the movement in the market can help you avoid the impact of short-term fluctuations.

Note: Major positive/negative events have been plotted.

1. Understanding it better

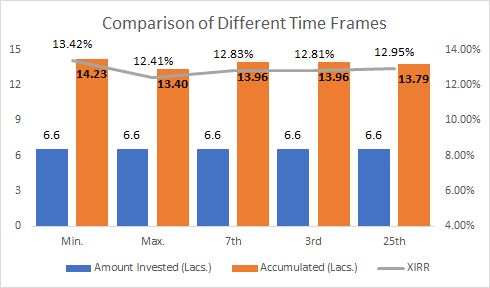

Let’s consider 5 situations where investors A, B, X, Y & Z invested ₹5,000 every month through SIP, for the past 11 years, in BSE Sensex as follows:

- Mr. A invests at the bottom/Min. of the market every month.

- Mr. B invests at the top/Max. of the market every month.

- Mr. X invests on the 7th of every month.

- Mr. Y invests on the 3rd of every month.

- Mr. Z invests on the 25th of every month.

| SIP Date | Min. | Max. | 7th | 3rd | 25th |

| Period | 11 Years | 11 Years | 11 Years | 11 Years | 11 Years |

| Amount Invested | ₹ 6,60,000 | ₹ 6,60,000 | ₹ 6,60,000 | ₹ 6,60,000 | ₹ 6,60,000 |

| Accumulated | ₹14,23,461 | ₹ 13,39,728 | ₹ 13,95,550 | ₹ 13,95,550 | ₹ 13,78,804 |

| XIRR | 13.42% | 12.41% | 12.83% | 12.81% | 12.95% |

Note: XIRR stands for Extended Internal Rate of Return. It is used to calculate returns on investment where there are multiple cash flows (e.g., SIP) taking place at different intervals.

IRR considers all the cash flows – both, inflows and outflows- and all the times at which these cash flows happen.

Note: The period under study is between Jan’11 to January ’21. Data for the BSE Sensex Index has been taken for calculating the SIP returns.

2. Time in the market matters more

Looking at the above returns, we can see that TIMING THE MARKET doesn’t really make much of a difference. It is also very difficult to time the market.

In fact, to be able to time the market correctly, you need to be a trader and not just an investor. Long-term investments should not be based on dates.

Instead of timing the market, try to remain invested for a longer period. Focusing on early investing is also as beneficial as staying invested for a long period.

This is because compounding adds value to your investment journey.

3. Understanding long-term investing

Long-term investing helps mitigate short-term risk & fluctuations in the market and can be rewarding over the long term.

Long-term investing is based on compounding and the rupee-averaging cost. Read on to learn a little more about these two terms.

4. What is compounding?

Compounding means you not only receive the returns on the amount that you have invested but also on the returns that keep getting added to your invested amount.

In investing, compounding acts as a multiplier in your investment portfolio. The great thing about compounding is that you will eventually reach a point – where the number of returns that are reinvested will become more than the originally invested amount.

All you need to do is start investing early & over time, compounding will grow your money for you. Let’s consider another example. Here Mr. C starts investing 5 years late. Take a look at what the returns will be below.

| SIP Amount | Period | Amount Invested | Accumulated | XIRR |

| ₹ 5,000/Month | 6 Years | ₹ 3,60,000 | ₹ 5,80,549 | 15.50% |

To achieve the target amount of 13.50 Lakh+, Mr. C needs to start a SIP of ₹11,500/Month.

If Mr. C had started investing 5 Years earlier, the SIP would have been 59% (₹5000/Month) less than the current SIP Amount. You can calculate your returns for multiple cashflows with XIRR.

Note: Considering Mr. C invests in BSE Sensex.

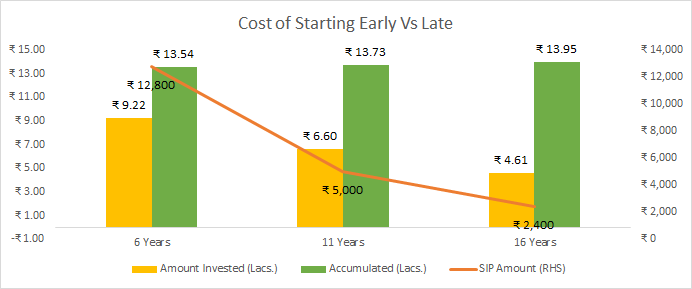

Lets’ understand what will be the impact on the SIP Amount & the Invested Value, by considering a target for the Accumulated Value as ₹13.50 Lakh+, if an investor starts 5 years early and another starts 5 years late.

| Period | 6 Years | 11 Years | 16 Years |

| SIP Amount | ₹ 12,800 | ₹ 5,000 | ₹ 2,400 |

| Amount Invested (Lacs.) | ₹ 9.22 | ₹ 6.60 | ₹ 4.61 |

| Accumulated (Lacs.) | ₹ 13.54 | ₹ 13.73 | ₹ 13.95 |

| XIRR | 12.00% | 12.00% | 12.00% |

Note: For the above calculation, XIRR has been considered as 12% p.a. The above is calculated using a normal SIP Calculator.

Look at the 3 scenarios above. The SIP amount and invested Amount have been drastically reduced to ₹2400/month for any investor who has started investing 5 years early.

For those who have invested 5 years late, the SIP Amount shoots up to ₹12800/month & the Invested Value is also the highest i.e., ₹9,22,000. So, one should start investing as early as possible, irrespective of the amount.

2. What is rupee cost averaging?

Rupee Cost Averaging is a concept in which you invest a fixed amount of money at regular intervals. This ensures that you buy more shares of an investment when prices are low and less when prices are high.

Over a period of time, the cost per unit averages out and usually places the investment in a perfect position to earn good returns.

One need not worry about timing the market as this approach lessens the short-term market fluctuations on your investments.

FAQs

Is timing the market better than time in the market?

Timing the market is better than time in the market is a cautionary investment tale. Is it better to time the market than time in the market – based on research, most people have had better results by staying invested for longer than by timing the market.

Is time in the market beat timing?

Timing the market can be tough for experienced and novice experts. It requires constant vigilance, market prediction analysis, and a deep understanding of the marketplace.

What is the biggest risk of market timing?

The biggest risk of market timing selling before or selling too late. It is difficult to predict a market high or low. Stock markets are notoriously unpredictable and require constant monitoring, analysis and a deep understanding of the stock market.

Conclusion

In conclusion, we’d recommend starting to invest early and remaining invested for a longer period instead of trying to predict the market.

Even experts cannot time the market. However, the earlier you start investing, the better. Investing early also adds financial discipline to your life.

Consult an expert advisor to get the right plan

recommended reading

10 Reasons Why You Should Study in the USA

4 essential tips on investing in your child's education

4 W’s of Balanced Advantage Funds

5 financial things to consider before child planning.

5 investment plans every parent should have

5 reasons why SIP is the best investment choice?

5 tips to know before investing in US stocks

5 top investments for risk-averse investors