Most of us grapple with the big question – how much % of our salary should we save and how much of it should we invest?

However, there is no thumb rule or fixed mantra for this (I really wish that there was). How much of your salary should go into your SIP entirely depends on your goals or the future expenses that you want to plan for. We would like to illustrate this by using some personas.

PERSONA 1 (Details in the table)

| Name | Hari Krishnan |

| Age | 25 |

| Salary (per month) | INR 40,000 |

| Family Details | Unmarried. Plans to get married in the next 2 years |

| Plans for future (Expected Expenses) | Wedding Expenses – 10 lakhs Education Expense for kids – 30 lakhs (Above expenses are according to the current level of expenses) Total expected expenses = 40 lakhs |

| Inflation | Inflation = 6% Educational Inflation = 12% |

Hari has lifestyle expenses which include rent, food, clothing, etc., which would add up to 30% of his salary, which would be Rs 13,500.

Also, he has taken a vehicle loan for purchasing a car for his parents and contributes 10% of his income to the EMI/loan repayment, which would be Rs 4500.

The expenses that are foreseeable in the future are education and wedding expenses. Assuming the inflation rates as mentioned in the above table, the expenses would be as follows:

| Expenses | Rate and Corpus required | Number of years |

| Wedding Expenses – Economy Inflation | 6% | |

| Marriage expenses | INR 11,91,016 | 3 |

| Educational Inflation | 11% | |

| Education Expenses | INR 2,41,86,935 | 20 |

| INR 4,07,56,391 |

As the wedding expenses are due in a shorter time frame, he can invest in short-term debt funds which offer an average return of 9% per annum, which would beat the inflation of 6% and offer him better returns than the fixed deposits in a financial institution.

For education, which is investing for a longer time frame, he can cultivate a discipline of saving every month to keep up with the constantly evolving dreams of a child and to have enough corpus to fulfill the dreams of his child, how much of his salary should he invest into a mutual fund?

Follow the calculations in the following table. A regular Equity Mutual Fund promises a return of 12-15%. Taking an average to be 13.5% –

| Monthly Saving | 19,702 |

| Expected Return | 13.5% |

| Time period | 20 |

| Maturity Amount (As calculated in the above table) | 2,41,86,935 |

Hence, Hari would have to save Rs 19,700 of his salary into an equity mutual fund to create a corpus of Rs 2.41 Cr for his child’s education.

He would be still left with Rs 7000 after excluding his lifestyle expenses and his investments.

As a parent, we should start as early as possible to ensure that we do not burden our child with a mountain of interest payments and principal payments from his or her educational loans.

It is our responsibility as a parent to provide a stress-free and debt-free life for our children.

| Name | Rajat Bhattacharya |

| Age | 45 |

| Salary (per month) | INR 70,000 INR 50,000 (Wife’s Income) Net Family Income = INR 1,20,000 |

| Family Details | Married with two children (Ages 12,15) |

| Plans for future (Expected Expenses) | Children’s Wedding Expenses – 20 lakhs per child Education Expense for kids – 30 lakhs per child (Above expenses are according to the current level of expenses) Total expected expenses = 100 lakhs |

| Inflation | Inflation = 6% Educational Inflation = 12% |

PERSONA 2 (Details in the table)

The following could be the monthly inflows and outflows of the family –

| Salary | 120000 |

| [-] Lifestyle expenses (Food, rent, clothes, celebrations, travel, etc) 40% of Salary | 48000 |

| [-] EMI (Loan payment) (6% of Salary) | 6000 |

| [-] Invest for Future expenses | ?? |

The future expenses can be detailed as follows –

| Expenses | Rate and Corpus required | Number of years |

| Wedding Expenses – Economy Inflation | 6% | |

| Marriage expenses | INR 85,31,713 | 13 |

| Educational Inflation | 11% | |

| Education Expenses | INR 1,38,27,227 | 8 |

| Total Corpus Required | INR 2,23,58,940 |

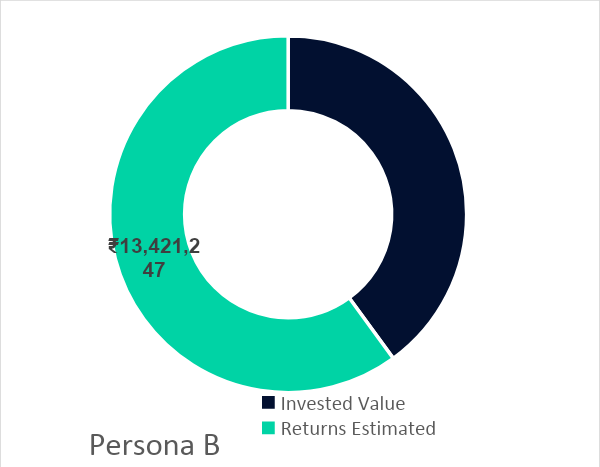

Assuming that Rajat invests in an Equity Mutual fund for the long-term expenses of the wedding and education of his children, which earn a return of 12%-15% per annum.

How much would his family have to save to ensure that they have a large enough corpus to cushion the future of their children?

| Monthly Saving | INR 62,067 |

| Expected Return | 13.5% |

| Time period | 12 |

| Maturity Amount (As calculated in the above table) | INR 2,23,58,940 |

In both personas, the estimated returns offer a higher benefit and enable a smooth sailing journey to reach your destinations.

Start early and reap the benefits of compounding. Also, do not shy away from equity markets. Index funds and other mutual funds charge a premium to manage your money to offer you a promised return.

They can be considered as one of the best financial products for long-term investing to reach your milestones in life.

FAQs

Should I invest 20% of my salary?

There is no fixed percentage that you should invest in a given year. Based on your needs and aspirations as well as budget, one can determine the available investment percentage from their income.

Most investors ideally follow the 20-30-50 rule wherein 20% is for investing, 30% for savings, and 50% for spending.

What is the 15x15x15 rule in mutual funds?

A popular rule to become a crorepati via investing in just 15 years. If an investor decides to invest 15,000 rupees every month for the next 15 years assuming 15% returns from his/her investments then there is a high chance you will be able to earn a crore.

How much of the salary should be invested in equity?

Ideally, one should invest 20 to 30% towards equity investment from their salaries. Starting early and taking advantage of compounding interest can