In the age of growing volatility across financial products, currency fluctuation over the years has been no different. The Indian rupee also had its share of wild fluctuations against the US Dollar.

For the ones who are not aware – Indian Rupee has depreciated to the tune of 61% in the past ten years, 11% in the past five years, and 4% in 2020 (year-to-date) against the US Dollar (all data as on November 30, 2020).

With the generation having global aspiration, such weakening local currency leads to higher pay-outs or direct losses when the liabilities are in US dollars, or the payments are in US dollars for the services availed.

A declining rupee against the USD is a spoilsport for Indians looking to travel abroad. It hits the budget of parents looking to send their children abroad for global quality education.

Not just that, the imports get costlier, which result in rising prices of gourmet and related items.

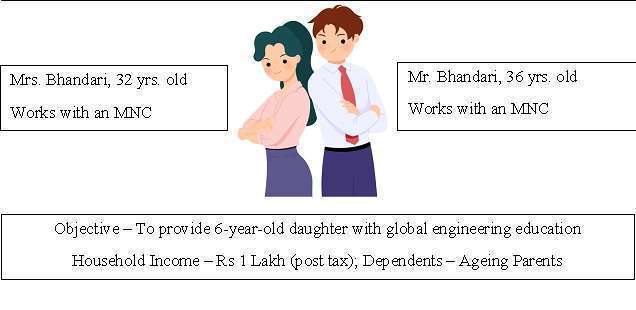

Let us understand this with the help of an example, a simple case study –

Let us assume, that Mr. Bhandari invests Rs 35,000 per month in Indian Mutual funds which are likely to generate 12% returns (annually). He also links his SIP to his salary increment and says that every year he will increase the investment by 7% (Step-up).

In this case, the amount accumulated in 12 years (the time left for sending his child abroad for education for a bachelor’s degree) is Rs 1.45 crore.

Let us now see how Bhandari can save using US assets. Assuming, Bhandari does a SIP of USD 500 every month and generates 11% returns (annually) while increasing SIP by the same value as before, he is likely to accumulate ~200K USD.

Now, since the cost of education or the tuition fees is to be paid in the USD, the accumulated corpus can help Mr. Bhandari pay the college tuition cost and cover some living expenses too which accounts for a sizeable cost in the total education expense.

Building dollar-dominated assets

We believe, that investing in foreign assets helps the individual diversify their portfolio to cover the risk associated with volatile/fluctuating economic conditions in their home country.

This is achieved because the investor tends to spread out the assets across geographies rather than sticking to conventional asset classes like domestic equities, debt, and commodities.

It is always advisable to have some investments in international stocks or assets.

Let us now compare the returns from the dollar and Indian indices –

Over the past ten years (as on Nov 30, 2020), the INR has depreciated by 61% (~5% CAGR) in terms of the US Dollar. At the same time, the US market has grown 169% (10.4% CAGR).

Compare it to S&P BSE Sensex – which during the same period has grown 126% (8.5% CAGR).

Even if India outperforms foreign markets, the lack of perfect correlation between different markets reduces portfolio risk.

Are you worried about the small portfolio including a foreign asset class?

You don’t need to worry if your portfolio is relatively small. You can always invest in foreign stocks through a mutual fund registered in India or through US ETF, which is made very simple with the help of digital transactions.

Investing in foreign assets shifts risk and acts as insurance against any wild swings that the domestic market may see. Under the liberalized remittance scheme (LRS), Indian residents are allowed to invest up to USD 250,000 annually in foreign stocks, bonds, and ETFs.

While the money transfer to a foreign broker has involved a bank branch visit, however, the FinTechs in the space are gradually easing up the process by offering pickup and drop services for transfer forms.

Besides, banks such as ICICI Bank allow a completely online process for transfers up to $25,000 – 10% of the total LRS limit.

This has made investing simpler for people who aspire to invest in US Dollar as a class. It typically will help people looking to travel abroad, and/or looking to send their child abroad for education.

Conclusion:

Building your corpus whether it be to settle abroad or send your children for education is a step that you have to take in order to secure yourself your child’s future.

Remember that planning fares well and your financial future is for you to build. So plan, strategize and invest wisely.

FAQs

Should I save in dollars or rupees?

Given the continued rupee depreciation against the dollar, buying US stocks from India can be beneficial for Indians in the long run. In fact, for parents who are saving for their child’s future foreign education, saving in dollars would be better.

How can I invest in US ETFs from India?

Investing in US ETFs is now at your fingertips. Just download the EduFund App ➡️ Create an investor account by completing your KYC verification ➡️ Explore your options and start investing.

What are dollar-denominated investments?

Transactions priced in USD, securities, and assets are some of the dollar-denominated investments.