The Nifty 50 has experienced a correction of over 10% from its all-time high. After making an all-time high of 26,277.35 on September 27, 2024, it plunged to 23,263.15 on November 21, 2024, before closing at 24,708.40 on December 5, 2024. This marks the first time the market has corrected by more than 10% since the Covid-19 crash.

Now, important questions arise for investors:

- Is the worst behind us, or could further declines be on the horizon?

- Have we reached the market bottom?

- And what insights can we draw from past corrections?

- How frequently have markets corrected by more than 10%, and how long did it take for them to recover?

Let’s explore these questions and see what history can teach us.

Understanding Market Corrections

Market corrections are a natural part of the investment cycle, often following a strong bull run. Typically, markets rise, peak, dip, bottom out, and then rise again – a continuous cycle. That’s why we often say that every bull run is followed by a correction, and every dip is followed by a pullback. In the short run, nothing is permanent – neither the upward momentum nor the downward pull. At times, markets may even trade within a defined range, and it often takes a strong catalyst to break this pattern. Interestingly, after a period of strong momentum, even a small piece of news can trigger a correction. Let’s now take a closer look at the potential reasons behind this market correction.

What are the reasons behind this correction and the volatility?

There can be several factors contributing to the current market correction. Let’s break them down one by one:

- Strong Bull Run – Indian markets have experienced significant growth since the Covid-19 crash, with little to no substantial corrections in recent years. After such a strong bull run, a correction becomes almost inevitable as markets need to adjust and stabilize.

Source – tradingview.com

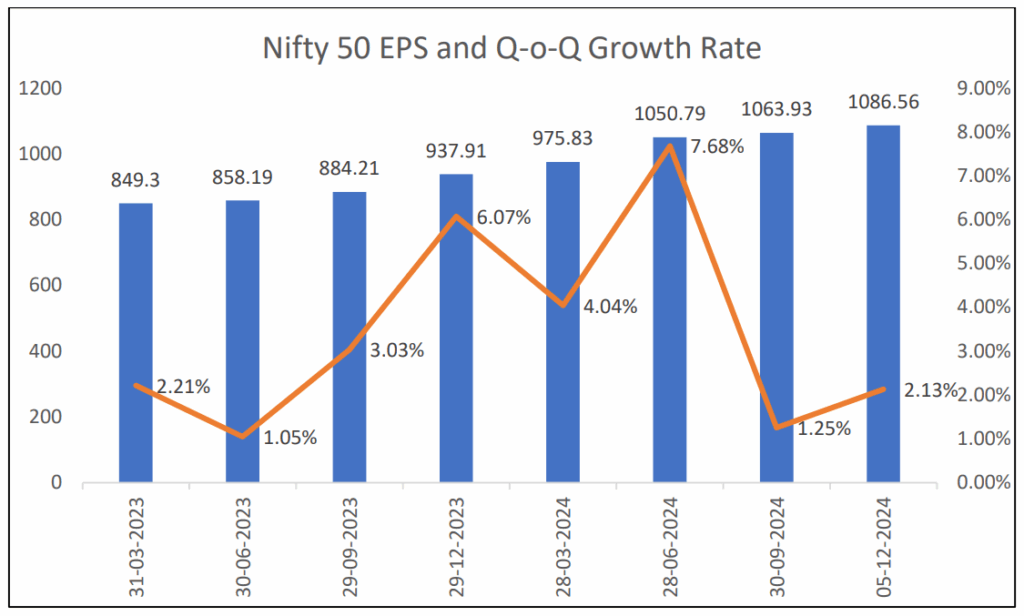

- Weak Corporate Earnings – Subpar corporate performance in Q2 has also played a key role in the market correction. Many Indian companies reported weaker-than-expected earnings, with more than half of the Nifty 50 companies missing analyst expectations. This tepid performance has dampened investor sentiment, contributing to the recent downturn.

Source – trendlyne.com, EduFund Research

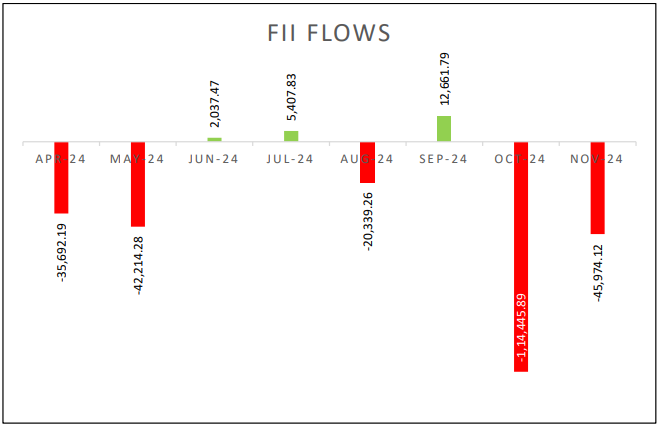

3. Strong FII Outflows – Foreign Institutional Investors (FIIs) have been significant sellers in the cash market, contributing heavily to the correction. As of November 30, 2024, total FII outflows for FY 2025 exceeded ₹2 trillion. To put this into perspective, the combined selling in October and November alone is more than double the net outflows recorded between April to September. This large-scale selling has increased pressure on the markets, leading to further declines.

4. Strong FII Outflows – Foreign Institutional Investors (FIIs) have been significant sellers in the cash market, contributing heavily to the correction. As of November 30, 2024, total FII outflows for FY 2025 exceeded ₹2 trillion. To put this into perspective, the combined selling in October and November alone is more than double the net outflows recorded between April to September. This large-scale selling has increased pressure on the markets, leading to further declines.

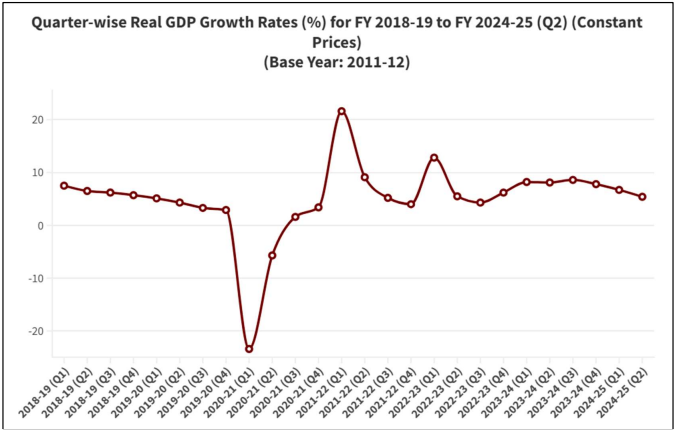

Source – MOSPI

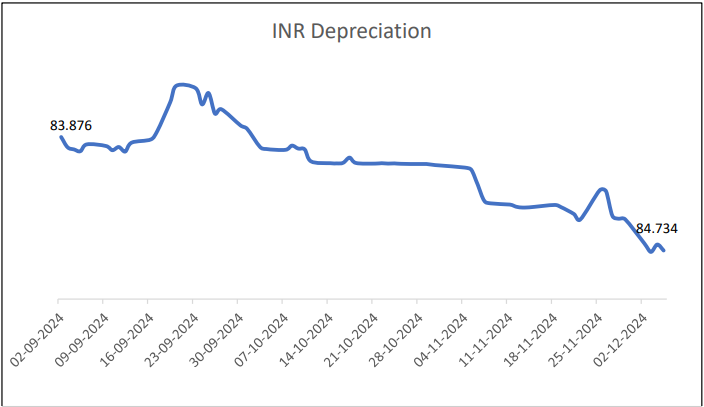

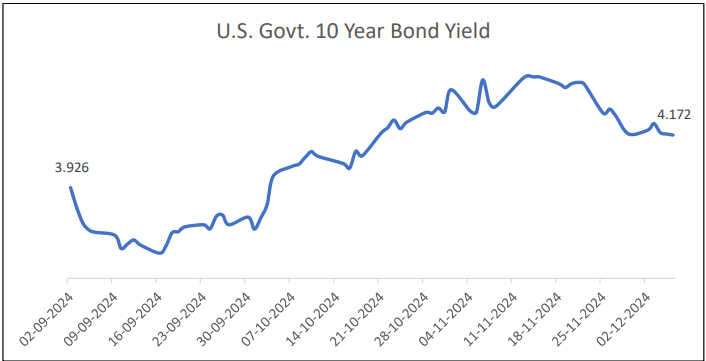

5. Other Factors – A combination of various global and domestic factors has contributed to the dip in investor confidence. The depreciation of the Indian Rupee against the U.S. Dollar and the rising bond yields in the U.S. have added pressure on the markets. Simultaneously, the economic slowdown in regions like the Eurozone, China, Japan, and Australia has raised concerns about global economic growth. The recent U.S. Presidential Elections introduced further volatility, while geopolitical tensions, particularly between Israel and Iran, as well as Russia and Ukraine, have heightened uncertainty. It is the interplay of these factors that has ultimately led to the current market correction.

Note – Chart based on inverted scale. Source – RBI

Note – Yields in percentages Source – investing.com

What does history tell us?

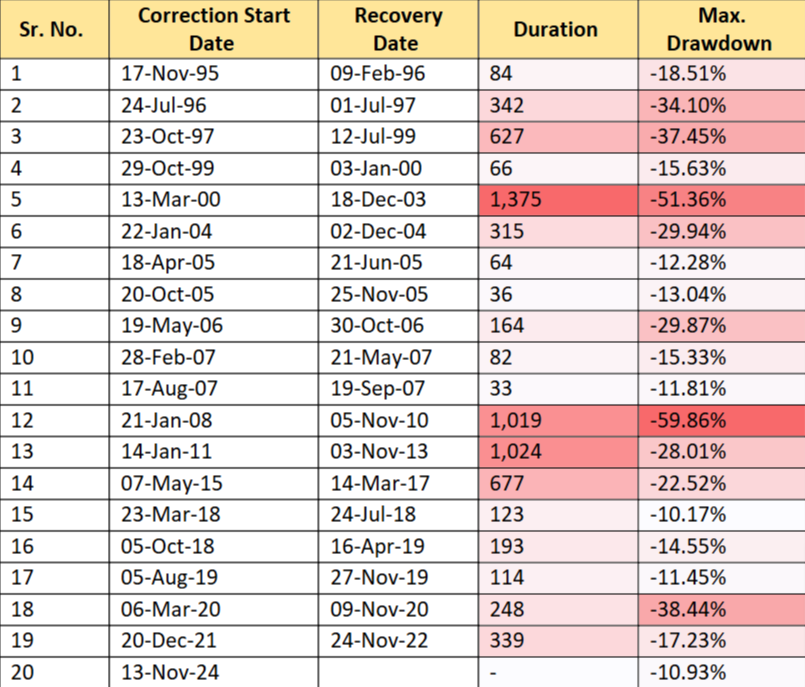

If we analyse Nifty 50’s performance since its inception on November 17, 1995, the index has corrected by more than 10% from its peak 20 times. On average, it has taken 364 calendar days to recover back to its previous high.

The longest recovery period was from March 13, 2000, to December 18, 2003, when the index took 1,375 days to reclaim its peak. Meanwhile, the correction triggered by the subprime crisis between January 21, 2008, and November 5, 2010, resulted in the sharpest drawdown of 59.86% from the peak.

The following table summarizes the key details of each correction:

Note: Correction Start Date marks when Nifty fell over 10% from its peak, and Recovery Date is when it reclaimed the peak, based on closing prices.

Source – niftyindices.com, EduFund Research

Is the Market Bottomed Out?

Since hitting a low of 23,263.15 on November 21, 2024, the Nifty 50 has shown a steady upward trend, closing above 23,300 consistently. As of December 5, 2024, the index closed at 24,708.40, marking a recovery of 1,444.99 points from its recent low.

One possible catalyst for this pullback is the decisive mandate received by the BJP-led Mahayuti in Maharashtra, which boosted investor sentiment. However, the underlying concern remains—corporate earnings and profitability, the key drivers of stock prices, are still under pressure.

The RBI’s dilemma between controlling inflation and supporting slowing GDP growth adds further uncertainty. Additionally, global factors like the Federal Reserve’s upcoming meeting and potential rate decisions will also influence market direction.

Given these factors, it’s challenging to definitively say whether the market has bottomed out. Volatility may persist until greater clarity emerges, particularly when Q3 earnings are announced in January, shedding light on profitability and cash flows.

What should a retail investor do?

Market corrections are a natural part of the investment journey—they’ve happened before and will happen again. However, the long-term growth story remains intact. Despite the recent slowdown, India continues to be one of the fastest-growing economies, and this growth is expected to translate into higher profits and stronger cash flows for India Inc. over time. To reap the benefits of this story, one needs to stay invested for long term.

Systematic Investment Plans (SIPs) offer a disciplined approach, allowing investors to benefit from rupee cost averaging during volatile times. Those with higher cash balances can consider investing in tranches during market dips or park funds in liquid or arbitrage funds and systematically transfer them into equities over time.

Regardless of strategy, the key to navigating market corrections lies in sticking to quality investments, maintaining diversification, and managing risk effectively.

Should you have any queries, feel free to reach out to us at research@edufund.in

Disclaimer

The data in this presentation are meant for general reading purpose only and are not meant to serve as a professional guide/investment advice for the readers. This presentation has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Investments in securities market are subject to market risks. Please read all the scheme related documents carefully.