Planning your finances as a parent is the most crucial yet underrated aspect of raising children. Amidst all your parental responsibilities, becoming a parent is emotionally and financially life-changing. One fine day, you suddenly are responsible not only for yourself but also for another person.

Embarking on this new adventure requires certain preparations. So, let’s figure out how to plan your finance as a young parent!

Financial hacks to learn on your new parenthood journey

Here are some hacks that will allow you to spend quality time with your newborn while managing your finances effectively.

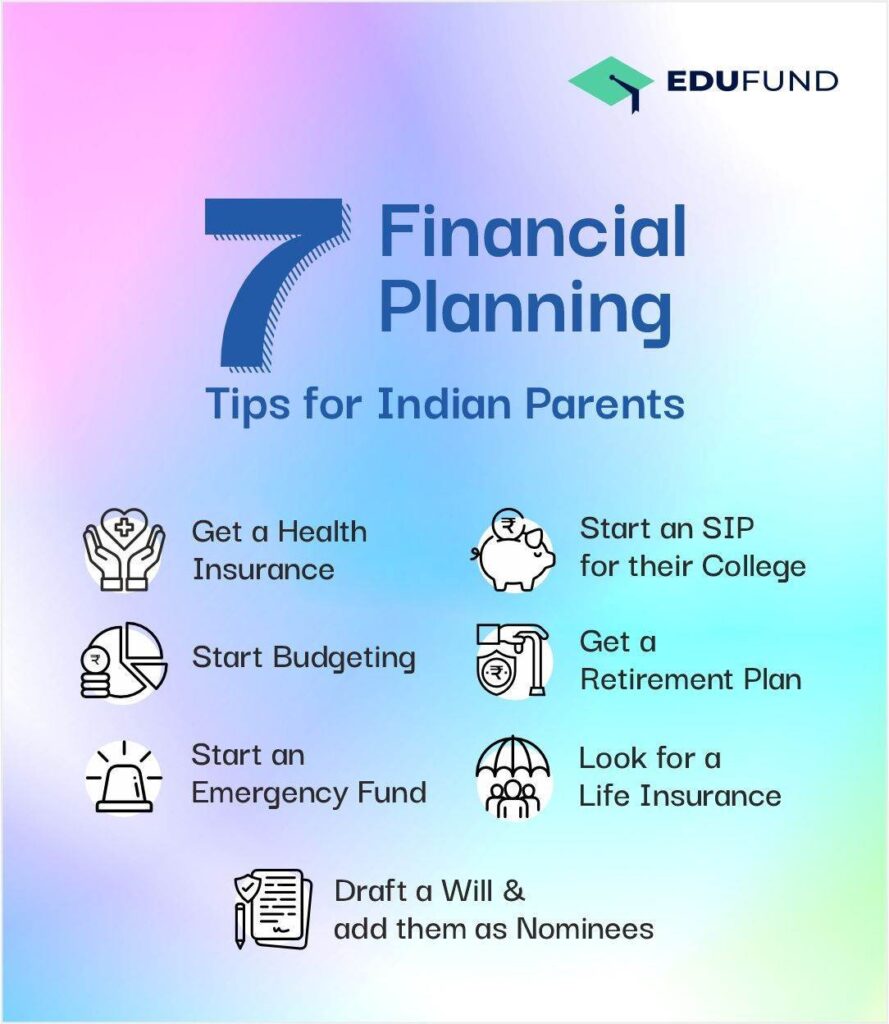

#1 Get a health insurance plan for your newborn

The most important step after your child is born is to update your health insurance plan or get a new one to cover your newest member. Many health plans allow young parents to add their child within 30-60 days after the delivery to the family health plan.

The insurance covers medical expenses, and hospitalization of the newborn baby and reduces the financial stress of medical bills!

#2 Create a Budget

With an infant entering your life, you will have new expenses. Diapers, baby clothes, baby food, and other childcare costs might add up quickly.

Besides, you would also have post-natal and prenatal medical expenses. Some expenses, such as new toys and diapers, might be recurring, while others, like a car seat and a stroller, are a one-time investment.

One quick note: It’s best to understand the “upfront costs” that might be a temporary hit to the wallet. Differentiate it from the recurring costs because they will influence your overall budget. You may also use online budgeting apps to alleviate further stress and anxiety.

Ways to invest in 2023

#3 Create an emergency fund

Sudden unemployment or hospitalization can be financially-stressful when your family is growing. That is why having an emergency fund covering between 6 and 12 months of living costs is valuable.

The emergency fund offers a comfortable cushion for new parents. Such a fund is crucial when your family relies on a single source of income.

#4 Save for your kid’s education

Surveys suggest that the average tuition & fees for private institutions were more than $30,000 during 2017-2018. According to research, only 13% of parents place college savings as the top child-related financial priority.

Even if your kid’s education does not sound like your immediate priority, the sooner you prepare for it, the better it is. You can start saving your money as per your salary to keep some amount for your child’s education.

#5 Financial plan for your retirement

With so many things to do for your infant, you might at times forget to prioritize your own life goals. But you must not undermine your priority. Just as your child is important, your future life is nowhere less significant.

You must consider setting up automatic withdrawal of retirement contributions. Prioritizing your retirement will prepare you for the future.

#6 Invest in a term life insurance plan

Like other insurance forms, life insurance also can financially protect you & your family against any worst situation.

You might not realize it, but term life insurance policies are extremely affordable. For healthy adults, these policies can cost less than monthly video or music streaming services.

The best part of investing in such an insurance policy is that it provides the financial protection that your family requires in case of any unexpected tragedy.

Due to the amount of coverage that varies by different aspects, life insurance calculators help determine the appropriate coverage for your family.

#7 Make a will & mention beneficiaries on your accounts

In the event of your unfortunate demise, financial arrangements for your child are crucial. A will, thus, offers a plan for the division of your assets. In addition, it also designates a legal guardian for your child.

Most individuals mention their surviving spouse or children as their account’s beneficiaries. You may select a separate guardian who can manage your accounts & assets until your kid reaches legal age.

An authenticated will helps avoid long legal battles about who owns your accounts & assets. It also helps define how your kid will be cared for. You may change the will & beneficiaries at any point in time.

One quick note: When you file out the essential forms, always take legal consultation from an attorney.

Ensuring these steps can safeguard your and your child’s future. Comprehensive financial planning as a parent can help you manage different expenses and maintain a healthy lifestyle for your family.

FAQs

Why is financial planning important for parents?

Financial planning for parents is a must. It helps them manage their child’s big and small finances – the biggest finance is education.

From nursery to college, Indian parents bear the cost of education, and it’s important to plan for its expenses. By categorizing and budgeting, parents can know how much they need, by when they need it so that they can start preparing for it.

For instance, the cost of engineering in India is nearly 4-5 lakhs today; in the next 5 years, this cost will double. So to save up for a child’s degree, you can choose mutual funds or US ETFs.

How do I financially prepare for my child?

Here are 7 ways to financially prepare for your child:

- Get a health insurance plan for your newborn

- Create a Budget

- Create an emergency fund

- Save for your kid’s education

- Financial plan for your retirement

- Invest in a term life insurance plan

- Make a will & mention beneficiaries on your accounts

How do I plan finances for my family?

The best way to plan your finances as a family is to create multiple budgets. You can have an annual budget, a 5-year financial plan, and a 10-year financial plan.

This will help you assess when you need to meet certain goals and how you can achieve the. You can consult a financial advisor to figure out the best possible route.

What are the five importance of financial planning?

Financial planning for parents helps in achieving the 5 most common goals: buying a home, children’s higher education, children’s marriage, retirement planning, estate planning, etc., and long-term financial security.