What is a Mutual fund?

Mutual funds are investment vehicles that pool money from a large set of investors and invest this net corpus into various asset classes such as government securities, corporate bonds, stocks of companies, money market instruments, etc., to earn the promised returns to its investors.

Fund manager who plays the role of the driver to the investment train and channels the pool of investments to align with the investment mandate and objective.

Multiple schemes are launched by Asset Management Companies (AMCs) or fund houses to match the investment objectives of various investors.

Why are mutual funds better than direct equity?

Direct equity or investing in stocks all by yourself requires a detailed study of the company, its business, financials, quarterly earnings, expected growth, and all the recent news updates around the industry and company to make an informed choice.

Investing in stocks gives flexibility to the investor to pick and invest in the companies and the sectors. However, the probability of a loss or risk is also very high in these investment vehicles, which is also coupled with a prospect of high return.

Investors with a deep knowledge of the markets balance the risk and return of their portfolios, but for the rest of the pool of investors, mutual funds are the most convenient vehicles for investment.

These vehicles also provide the diversification required to satiate the risk appetite of the investor by investing in various asset classes, and in various sectors within the asset class in a portfolio.

Advantages of Mutual Funds

1. Low ticket size, with good returns

Some of the shares of Bluechip companies have high prices, which often tend to be inaccessible to the investor. For example Hindustan Unilever Ltd, the leading FMCG company has a stock price of around Rs 2400.

An investor who has a lower ticket size of investment of Rs 500 or Rs 1000, would find this lucrative stock to be out of his/her investment orbit.

However, with mutual funds, one can buy units of the fund starting from Rs 500, which invests into these companies with the pool of money collected from the investors, hence providing every penny with diversified returns.

2. Professional management

Mutual funds offer the expertise and an army of research analysts who perform a detailed study of the market conditions, industry outlook, company’s business, and financials and make an informed decision of investing the pool of money to earn the best returns.

Everyone does not have the time and the knowledge to perform research and identify the right stocks and mutual funds to provide these services on a platter!

4. Liquidity

Liquidity indicates the ease of entry or exit into any instrument. For example, Company A, a renowned company with strong financials is traded more frequently than Company B, a stock of an underperforming company, implying that the stocks of Company A are more liquid and easier to trade than Company B.

Similarly, mutual funds are also liquid instruments, where an investor can buy units of the fund, and in an open-ended fund, he/she can sell the shares at NAV (Subject to exit load conditions of the fund).

This ensures that the investor gets fair value for the units/shares of the fund.

5. Management of risk

As individual investors, we often lack the expertise to assess the risk of our portfolio. We could also put all the eggs in one basket and lose our hard-earned money overnight.

However, AMCs have risk management guidelines that limit or restrict the fund manager’s investments in some sectors and stocks.

This ensures that the risk in the portfolio is well calculated and within the limits as promised to the pool of investors.

The fund could also invest in various asset classes – bonds, commodities, stocks, gold, etc, which not only aids in diversification but also in gaining from the high potential returns from the asset classes.

The fund manager’s decisions are also backed by strong research and analysis of each sector, asset class, and the conditions of the economy.

6. Choice or variety of funds

Each of us has a different personality. Some of us are aggressive with our investments and can withstand a certain percentage of volatility, whereas some of us are risk-averse investors who cannot stand the thought of losing our money.

Mutual funds are available that are approximately tailored to our risk profiles. For example, an aggressive investor can choose a diversified equity fund, whereas a risk-averse investor could choose to invest in a balanced fund.

7. Taxation

Mutual funds offer indexation benefits for being invested in the fund for more than a year, which finally results in tax-free gains.

7. Transparency

As an investor, you can see where your money is being invested. The strategy for investing is publicly declared by the fund.

The NAV also updates daily, giving a lucid picture of the investment value to its investors

How can mutual funds help in saving for education?

Saving for your child’s education can be a daunting task, given the rising cost of education. In our previous generation, our parents depended on FDs, gold, and PPFs to fund our education, but the returns from these asset classes would not be sufficient to beat the current educational inflation.

Investment in equity would be the best route for grabbing the maximum returns over every penny. However, investing in direct equity requires detailed analysis and research coupled with the volatility of the asset class.

Mutual funds would be the one-stop solution for all your long-term goals providing you with financial discipline (through SIP) and also providing the required returns to beat inflation.

If the child wants to pursue his/her higher education in a reputed college for costing around INR 25- 28 lakhs today, it will multiply to a much higher amount of over INR 1-1.5 cr in the next 15 years, given the educational inflation around the globe.

To save for this scenario one would have to invest approximately Rs 15,000 – Rs 22,500 per month to accumulate the final corpus.

One could also rely on an educational loan in the future but could accumulate 60% of the required corpus by investing Rs 9000 per month as a SIP into the fund.

| 1 Cr | 1.5 Cr | 0.6 Cr | |

| Monthly saving required | 14,959 | 22,438 | 8,975 |

| Expected return rate | 15% | 15% | 15% |

| Time Period | 15 | 15 | 15 |

| Maturity amount | 1,00,00,000 | 15000000 | 60,00,000 |

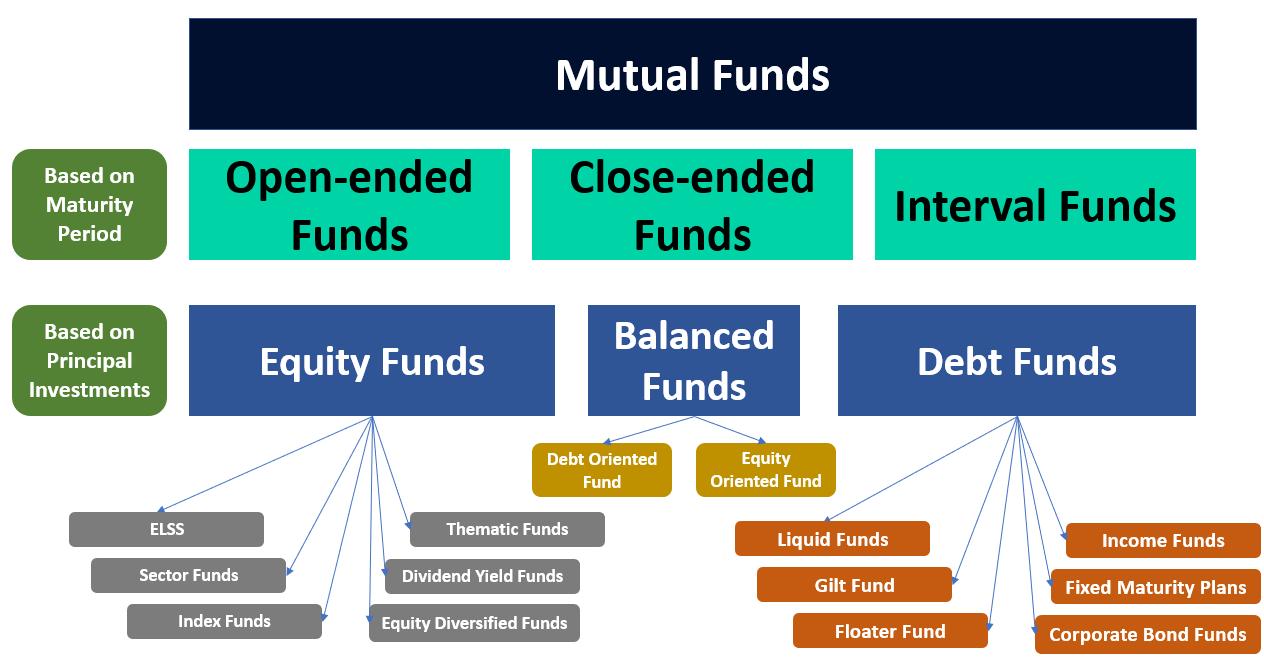

Types of Mutual Funds

A plethora of options of mutual funds is available in the market, which allows the investor to choose based on the investment horizon, risk appetite, amount for investing, etc.

The funds are categorized into the following types based on the –

- Principal Investments

- Maturity Period

a) Maturity Period Classification

1. Open-ended funds

The majority of the funds (approximately 59%) are open-ended. These provide the flexibility to buy and sell units of the fund at any point in time.

There is no maturity period. It is like buying a stock, where you transact at the Current Market price – in mutual funds you buy and sell units at NAV.

There is no exit load (subject to lock-in conditions). The key feature of these types of funds would be liquidity.

2. Close-ended funds

These funds have a maturity period (of 3-5 years). Investors can have an entry into the fund only at the time of the New Fund Offer (NFO). However, the exit has two routes –

Sale of units through the stock exchange: In the case when the investor needs to withdraw the amount, he/she can sell it on the exchange.

However, this route could be illiquid, as one may not find enough buyers for the sale of the unit and could also result in a potential loss (by selling the units at a lower price)

The second exit route is at maturity. Some mutual funds give the option to sell and exit the fund through the periodic repurchase of units at NAV

3. Interval Funds

These funds have the characteristics of both open and closed-ended funds, where the fund allows the purchase/sale of units at pre-defined intervals.

b) Principal Investments Classification

1. Equity funds

These funds invest in Equity and equity-related instruments. The fund manager aims to beat the market/benchmark by spreading across various sectors or by picking companies across different market capitalizations.

They earn more returns than the Debt and Hybrid schemes. SEBI has defined 11 categories of these funds. It has also defined the variation between the categories as follows:

- Large-Cap: First/Top 100 companies in terms of Market Capitalisation

- Mid-Cap: 101-250 companies ranked according to Market Capitalisation

- Small–Cap: Companies ranking above 250 with respect to Market Capitalisation

2. Debt Schemes

These funds invest in fixed-income securities such as Government Bonds, Corporate bonds, commercial papers, and other money market instruments.

The maturities of these are fixed, implying that the returns are unaffected by the fluctuations in the market if held until maturity.

These schemes are hence considered less risky when compared to the Equity Schemes. SEBI has defined 16 categories in these funds.

3. Hybrid Schemes

These schemes invest in a combination of debt and equity to create a specific investment objective. Each hybrid fund has a different % of the allocation to debt and equity.

- Equity Oriented

These invest >65% in equity and equity-related instruments. The remaining 35% is invested into debt and other money market instruments.

- Debt Oriented

These invest >60% of assets in fixed-income instruments or debt instruments such as G-secs, bonds, debentures, etc. The remaining 40% is invested in equity.

4. Balanced Funds

These funds invest a minimum of 65% in equity and equity-related instruments. The remaining is invested in cash and debt securities.

For taxation purposes, these are considered equity-oriented funds where a tax exemption of Rs 1 lakh can be obtained on the long-term gains from the fund.

Conclusion

Having a financial discipline aids in having a corpus for all your long-term goals. Mutual funds act as a convenient vehicle for driving you to your financial destinations (goals).

As an investor one must consider their risk profile, investment horizon, goals, and investment amount before jumping into any fund.