When an ETF’s Volatility is taken into account, an investor may find it challenging to determine which fund offers the best risk-reward ratio.

Learn about the four most popular volatility metrics and how they’re used in different types of risk assessments here.

What is Volatility ETF?

Volatility is a parameter of how quickly the price of a security fluctuates over time. It expresses the degree of risk linked with a security’s price movements.

Investors and traders measure a security’s Volatility to assess past price fluctuations and forecast future moves.

Types of Volatility

1. Historical Volatility

The historical volatility indicator shows how the price of the security has fluctuated. It helps to forecast future price fluctuations based on historical trends.

However, it does not provide insight into the future direction or trajectory of the security’s price.

2. Implied Volatility

This is the underlying asset’s Volatility that will yield the theoretical value of an option equivalent (derivatives) to the option’s current market price.

In option pricing, Implied Volatility is a critical factor. It offers a forward-looking perspective on potential price variations in the future.

Most popular volatility metrics

Standard Deviation

The standard deviation measures an ETF’s Volatility or the likelihood for earnings to rise or fall dramatically over a short period. A volatile investment is one that poses a more significant risk since its performance can swing either way dramatically

The standard deviation of an Exchange Traded Fund assesses this risk by determining how much the fund varies from its mean return.

For example, a fund with a steady four-year return of 7% will have a mean, or average, of 7%. Since the ETF’s return in any given year does not depart from its four-year mean of 7%, the standard deviation for such an ETF would be zero.

An ETF that returned –15%, 17%, 12%, and 20% in each of the previous four years, on the other hand, would have an average return of 8.5 percent.

This fund would also have a significant standard deviation because the fund’s return departs from the mean return each year.

As a result, this fund is riskier because it swings back and forth between favorable and unfavorable returns in a short period.

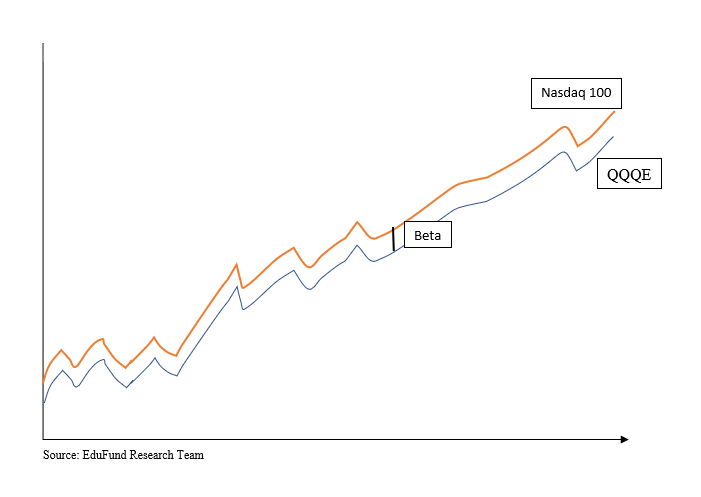

Beta

While standard deviation measures a fund’s Volatility based on the spread of its returns over time, beta, another relevant statistical measure, compares a fund’s Volatility (or risk) to its index or benchmark.

When a fund’s beta is very near to one, it suggests that its behavior closely resembles the underlying index or benchmark. A more extensive beta implies that the market is more volatile than the benchmark, whereas a beta below suggests that the fund is less volatile than the underlying benchmark

Let’s take a small example about the market; the lower the beta, the less susceptible the underlying instrument is. The QQQE has a beta of 1.04, according to ETF.com, which suggests that if the Nasdaq 100 rises by 1%, the ETF will climb by 1.04 percent.

Investors who anticipate a bullish market may buy funds with high betas, increasing their chances of outperforming the market.

If investors expect negative demand shortly, funds with a beta of less than one are a suitable pick because they might lose less than the benchmark.

R-squared

The R-squared of a fund tells investors whether an ETF’s beta is adequate compared to a benchmark.

R-squared explains the degree of association between a fund’s fluctuation and market risk, or, more particularly, the extent to which a fund’s variability results from the general market’s day-to-day variations by calculating the relationship of a fund’s movements to those of an index.

R-squared values vary from 0 to 100, with 0 denoting no correlation and 100 representing complete correlation. If the R-squared value of a fund’s beta is near 100, the fund’s beta should be trusted.

An R-squared score near zero, on the other hand, shows that the beta isn’t very relevant since the ETF is being evaluated to an inadequate benchmark.

More than that, the beta will be skewed by an incorrect benchmark. Because alpha is determined using the beta, it’s best not to trust the number provided for alpha if the fund’s R-squared value is low.

Alpha

The amount of additional risk that enabled the ETF to outperform its matching benchmark is measured by alpha.

Using beta, alpha evaluates the fund’s return to the risk-adjusted returns of the benchmark and determines whether the fund outperforms the market, being consistent in terms of risk.

For instance, if a fund’s alpha is one, it exceeds the benchmark by one percent. Negative alphas are wrong since they suggest that the ETF underperformed for the fund’s investors’ additional, fund-specific risk.

These are some factors that should help you evaluate the risk associated with ETFs. However, one must also consider their risk appetite before investing.

FAQs

How do you calculate the volatility of an ETF?

The standard deviation measures an ETF’s Volatility or the likelihood for earnings to rise or fall dramatically over a short period.

A volatile investment is one that poses a more significant risk since its performance can swing either way dramatically.

The standard deviation of an exchange-traded fund assesses this risk by determining how much the fund varies from its mean return.

What is a good volatility ETF?

The standard deviation of an exchange-traded fund assesses this risk by determining how much the fund varies from its mean return.

For example, a fund with a steady four-year return of 7% will have a mean, or average, of 7%. Since the ETF’s return in any given year does not depart from its four-year mean of 7%, the standard deviation for such an ETF would be zero.

An ETF that returned –15%, 17%, 12%, and 20% in each of the previous four years, on the other hand, would have an average return of 8.5 percent. This fund would also have a significant standard deviation because the fund’s return departs from the mean return each year.

As a result, this fund is riskier because it swings back and forth between favorable and unfavorable returns in a short period.

What is a good volatility percentage?

The standard deviation of an exchange-traded fund assesses this risk by determining how much the fund varies from its mean return.

For example, a fund with a steady four-year return of 7% will have a mean, or average, of 7%. Since the ETF’s return in any given year does not depart from its four-year mean of 7%, the standard deviation for such an ETF would be zero.

An ETF that returned –15%, 17%, 12%, and 20% in each of the previous four years, on the other hand, would have an average return of 8.5 percent. This fund would also have a significant standard deviation because the fund’s return departs from the mean return each year.

How does a volatility ETF work?

A volatility ETF will move in the opposite direction to the popular stock market indices. When the stock market index moves up, the volatility ETF will decline.