![]() Fall 2024 Scholarship: Get Up to $10K for Your Master's Abroad!

Fall 2024 Scholarship: Get Up to $10K for Your Master's Abroad!

![]() Fall 2024 Scholarship: Get Up to $10K for Your Master's Abroad!

Fall 2024 Scholarship: Get Up to $10K for Your Master's Abroad!

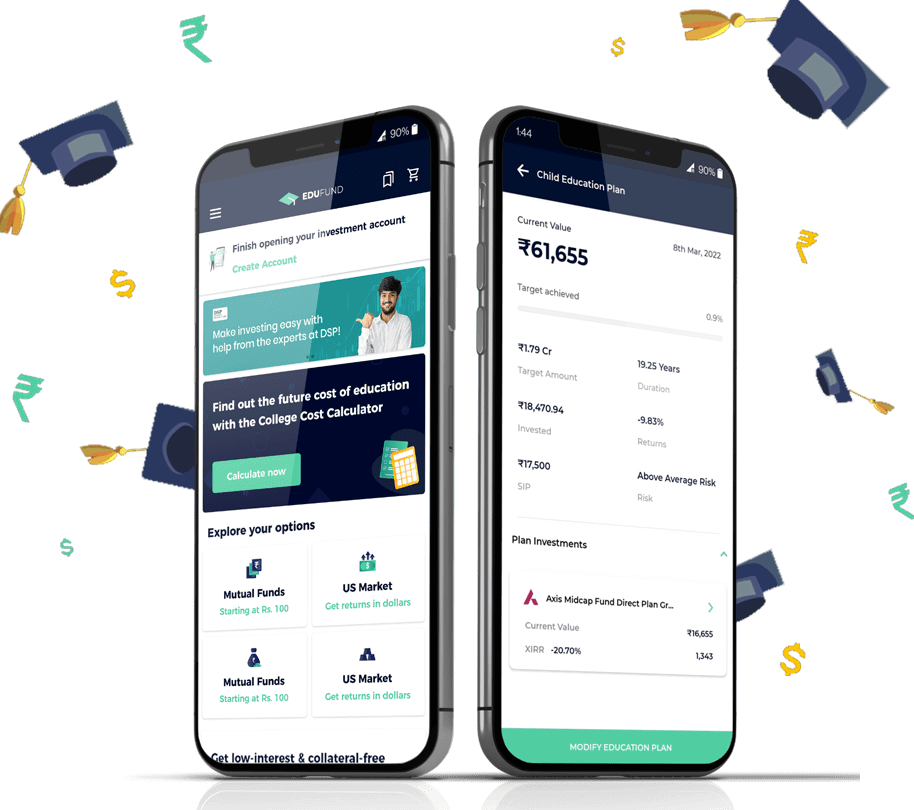

A degree that costs Rs.40 lakhs today, can cost approximately

Rs.80-90 lakhs in the future.

Find out exactly how much you will pay for college.

after Year

| Year | Amount Invested | Education savings |

|---|---|---|

| 2022 | ₹60,000 | ₹24,18,000 |

| 2023 | ₹60,000 | ₹32,59,000 |

| 2024 | ₹60,000 | ₹40,71,000 |

| 2025 | ₹60,000 | ₹52,98,000 |

| 2026 | ₹60,000 | ₹64,18,000 |

| Amount Invested | ₹36,84,360 | |

| Total Investments | ₹80,00,000 | |

Calculate

college

education cost

Start early

investments

Talk to Education

counsellors

Get quick

education loans

Graduate from

dream college

Calculate

college

education cost

Start early

investments

Talk to Education

counsellors

Get quick

education loans

Graduate from

dream college

Find out much you need for college

Learn more

Financial plan to achieve this goal

Learn more

Get help with college applications

Learn more

Get low-interest education loans with top banks

Learn moreUse smart savings plans to invest in your child's future

Grow your savings, save on taxes, opt for low risk & create wealth

Learn more

Save in rupees to get dollar returns

Learn more

Buy and sell 24k Digital Gold of 99.9% purity at live market rates

Learn more

Grow your savings with advice from qualified advisors

Learn more

No hidden costs and zero commission to help you save on unnecessary fees

Invest smart and save up to 1% more with direct plans.

SEBI-registered investment advisors to help you invest easily & smartly

The best thing about the EduFund app is that it allows me to plan and save financially, and it also offers a counselling feature. With a customized investing strategy, I’m confident that I can secure my little one’s future!

What we needed is expert advice and guidance. Thankfully, we came across a unique app called EduFund. For my daughter’s future, they offered a personalized financial plan. Plus, it’s so simple to set up an education fund.

This app is a game-changer! Seamless investing experience with EduFund. The level of detail and focusgiven is excellent. I’d highly recommend this to Indian parents.

What sets edufund apart from others is it focuses mainly on every new parent's confusion on investing and saving for their kid's future. Not only is the app user friendly and detailed but they have a very friendly and informative staff to support and follow up. I have grown my knowledge and interest in investing

Education has become so expensive. I wanted to be prepared for my children's college fees when the time comes. EduFund has helped me in planning for both my kid's college.

Our Investment Packs:

17.64%

Above Average Risk

By EduFund Advisory Team

11.97%

Average Risk

By DSP Advisory Team

Get a low-interest education loan with our partners-

Axis and ICICI

Get a low-interest education loan with our partners - Axis and ICICI

Learn more about being prepared for tomorrow financially

This website including the ‘[EduFund]’ platform is owned, operated and maintained by Helena Edtech Private Limited, a company incorporated under the laws of India. The platform and the services thereunder are provided on an "as is" basis. Use of the service and the platform is at your own risk. Company makes no warranty that the use of the service and the platform will be continuous, uninterrupted, bug-free, error-free, virus-free, free of defects, free of technical problems, nor that it will meet all of your needs. To the extent permitted by applicable law, Company expressly disclaims all other warranties, conditions, results, guarantees, or representations with respect to the service and the platform, whether express or implied, including, but not limited to, the implied warranties of merchantability, merchantable or satisfactory quality, fitness for a particular purpose, non-infringement of third party rights, or arising from the course of performance, course of dealing, or usage of trade.

Investment in securities market are subject to market risks, read all the related documents carefully before investing. The valuation of securities may increase or decrease depending on the factors affecting the securities market.

EduFund and the EduFund App are the brand and product of Helena Edtech Private Limited

An affiliate of the Company, i.e. Samyama Advisors Private Limited, is registered with the Securities and Exchange Board of India (SEBI) as an investment adviser under the SEBI (Investment Advisers) Regulations, 2013 bearing the registration number [INA000015321]. Samyama Advisors Private Limited may provide investment advice to the clients through the Company's platform.

An affiliate of the Company, i.e. Edubillions Tech Private Limited is registered with AMFI as mutual fund distributor bearing the registration number ARN258733

Registered Address: 30, Omkar House, Near Swastik Char Rasta, Navrangpura, Ahmedabad Gujarat, India – 380009

Transaction Platform Partner : BSE Star MF (with Member code-51573). CIN No: U67100GJ2020PTC112589. RIA Number: INA000015321 GST No: 24AAFCH2122L1ZU