Category Archives: Finance

What is AUM in mutual funds? All you need to know

What is AUM in mutual funds? What does it stand for or how is it calculate? Let's answer what does it mean when investors talk about AUM in mutual funds!

The aggregate market value of the investments held by a mutual fund is known as its Assets Under Management (AUM). On behalf of the investors, the fund manager handles these assets and makes all investment-related decisions.

AUM is a measure of a fund house's size and performance. The assets managed by a fund can be easily compared with other similar funds' performance over time.

The returns a mutual fund receives are also factored into the AUM value. This can be used to purchase securities, hold them as specified by the investing mandate, or distribute dividends to investors.

Things to consider in AUM before investing?

Investors in mutual funds frequently evaluate the fund's AUM and are impressed if it is on the higher side. People assume that a fund must be good if so many investors have previously contributed to it.

However, there are a lot of reasons why this number shouldn't matter when selecting a fund.

Some of the most crucial elements to consider are the expense ratio, the fund manager's reputation, and compliance with the investing mandate. Let's examine the significance of AUM in relation to various fund types.

1. Large-cap funds

Let's examine an example of how AUM affects large-cap mutual funds. Two large-cap equities funds are HDFC Top 200 and Mirae Asset India Opportunities.

The former's AUM is Rs.14,655 crore compared to the latter’s just Rs.4,738 crore. Most investors may choose to invest in HDFC Top 200 for this reason. However, the Mirae has historically earned higher returns over various periods.

2. Small-cap funds

Small-cap funds typically limit the inflow of cash after a specific threshold. A well-known case of this is the DSP BlackRock Micro Cap Fund.

This typically happens when a mutual fund's assets exceed a certain threshold.

When the market fluctuates, the fund might not be able to quickly trade its shares if it becomes a major stakeholder in a company.

Due to this, small-cap funds frequently stay away from lump-sum investments and instead opt for SIPs.

3. Debt funds

If you’re considering investing in debt funds, AUM is an important factor to consider. The fixed fund costs might be split among more investors in a debt fund with higher capital.

This can lower the cost per individual and hence boost fund returns.

Additionally, more assets under management assist the fund organization in securing fair interest rates from debt issuers.

4. Equity funds

Here, stability in returns and commitment to the investing mandate by the fund company is more important than AUM. By stability, we mean surpassing the benchmark during both the highs and lows of the market.

As a result, rather than popularity or size, an equity fund depends on the asset manager's ability to produce strong returns consistently.

How to calculate AUM in mutual funds?

Fund houses use different techniques to determine assets under management. When a fund continuously generates positive returns, its total investment value will increase.

Growth in AUM might result from the attraction of new assets and investors due to strong performance.

Similarly, assets may drop if the market value or investment performance declines. The same applies to sudden fund closures and share redemptions by investors.

Capital that has been invested in the firm's goods is included in its assets under management, which also includes the stock of the company's executives.

Formula to calculate AUM: "AUM = Net Asset Value (NAV) * Total number of units.”

AUM's impact on the expense ratio or fee

Every fund house charges a fee called a management fee that is based on the size of the fund. Investors are charged based on the number of units they own at a single cost for the entire fund.

The fees are unaffected by the performance of the fund.

It just pays for administrative costs and establishes the asset manager's pay for his work. The annual costs to run a mutual fund are measured by the total expense ratio (TER).

According to SEBI, the AUM must always be more than the TER.

source: pixabay

High AUM's effects on mutual funds

AUM growth can occasionally hurt an equity fund's performance. However, there is hardly any data to suggest that a bigger AUM either helps or hurts the fund's performance.

The fund manager is the one who should seize market opportunities and buy or sell a stock at the appropriate moment.

Larger assets under management have frequently made it more difficult for the manager to make rapid judgments regarding investments. Before investing, evaluate the fund's performance in relation to the benchmark and its rivals.

Higher AUM means the manager needs to be on point and well-experienced. Check the experience of the manager in handling high assets before investing in such funds.

AUM and market fluctuations

Market movements have a significant impact on the assets managed. The assets of the fund will increase when it generates returns and decrease when it suffers losses.

This impacts the mutual fund fee as well. Lower expenses typically equate to lower value.

For instance, imagine that a mutual fund that has produced 10% returns has received a total investment of Rs. 10,000 from 100 investors. If so, Rs. 11,000 would be the fund's AUM.

After all, businesses determine the worth of their assets under management using a variety of techniques.

AUM is a great way to evaluate a fund's popularity and performance. However, it should not influence your decision to invest in that fund.

Should you consider AUM before investing?

AUM is an essential factor that helps you in shortlisting the funds. The higher the AUM, the more stable the fund could be. Often you will see Analysts mentioning AUM > Rs 1000 crore is a good benchmark as it defines the fund's stability.

Also, the expense incurred to manage the fund gets spread, and the expense ratio reduces with rising AUM. Let us see the impact of AUM on equity funds and debt funds -

1. Equity funds

In equity funds, consistency and sustenance of returns are more critical than AUM. Thus, the investment process and philosophy should be given more importance.

2. Debt funds

In debt funds where the investment is in different fixed-income instruments, it is critical to consider AUM. While benefits such as expense ratio and reputation are one thing, the essential thing in debt funds is getting reasonable rates with debt issuers.

With higher AUM, the fund manager tends to get better rates which add to the performance. Also, higher AUM in debt funds for retail investors adds to the fund's stability.

Impact of high AUM in mutual funds

While a high AUM is good for the stability of the fund but huge AUM often impacts your performance.

For example - in the case of Large Cap Equity funds, if a fund reaches are very high AUM, the performance is likely to get impacted as the universe of stocks in which the money can be deployed is minimal and beyond a point outperforming the benchmark in large-cap space (where information inefficiency is negligible) is often tricky.

Thus, while AUM is necessary for the stability of a fund, it is not the only and single most critical factor on which the decision to buy or sell a fund should be dependent.

FAQs

What is a good AUM in mutual fund?

AUM is a measure of a fund house's size and performance. AUM size only matters in certain funds.

What is AUM vs NAV?

NAV refers to the prices of shares in a fund while AUM refers to the value of assets managed by the advisor.

How is AUM calculated?

Here is the formula to calculate AUM: "AUM = Net Asset Value (NAV) * Total number of units.”

Consult an expert advisor to get the right plan for you

TALK TO AN EXPERT

UTI Mastershare Unit Scheme

UTI Asset Management Company (AMC)

UTI is one of the pioneers of the Indian Mutual Fund Industry.

With over Rs 2.4 lakh crore, the AMC is one of the most trusted names in the mutual fund space. The AMF offers products across asset classes.

Let us talk about its flagship product – UTI Master share Unit Scheme

About Fund

1. Investment objective

The fund seeks to generate long-term capital appreciation for investors by investing in equity and related securities of large-cap companies.

It is India’s first equity-oriented fund launched in October 1986.

2. Investment process

The Fund takes a top-down view of the sector and then takes a bottom-up approach to select the stocks within the sectors. The fund is a well-diversified portfolio and avoids sector as well as stock concentration.

3. Portfolio Composition

The portfolio holds the major exposure in large-cap stocks at 87% and sectorally major exposure is towards financial services which account for roughly one-third of the portfolio. The top 5 sectors hold nearly 63% of the portfolio.

Note: Data as of 30th Sep 2022. Source: UTIMF

Top 5 Holdings

Name Sector Weightage % ICICI Bank Financial Services 9.52 Infosys Information Technology 7.12 HDFC Financial Services 6.12 Bharti Airtel Telecom 4.52 Reliance Oil and Gas 3.93 Note: Data as of 30th Sep 2022. Source: UTIMF

Fund performance over 35 years

If you would have invested 10 lakhs at the inception of the fund, it would be now valued at Rs 18.20 crore whereas the benchmark (S&P BSE 100) would have fetched you Rs 11.88 Crore.

Note: Performance of the fund since launch; Inception Date – October 15, 1986. Source: utimf.com

The fund has given consistent returns and has outperformed the benchmark over the period of 35 years by generating a CAGR (Compounded Annual Growth Rate) of 15.56%.

Now, let’s look at the fall of the fund during market corrections.

Source: utimf.com

The above table explains that the fund has seen less fall/correction compared to the market correction.

While corrections are painful for the short-term investor, at the same time, it is an opportunity to make higher returns for the long-term investors.

Fund manager

The fund is managed by Swati Kulkarni and Karthikraj Lakshmanan. Swati has over 36 years of experience and has been managing the fund since December 2006.

Karthikraj has over 17 years of experience and is a new entrant in this fund management.

Who should invest in UTI Mastershare unit scheme?

Investors looking to

Own large-cap businesses with sound management, steady cash flow, and earnings growth

Build core equity portfolio for long-term wealth creation with steady growth

Why invest in the UTI Mastershare unit scheme?

India’s first equity-oriented fund with a proven track record of over 35 years and over Rs 10,000 crore in Assets Under Management currently.

Strong stock selection approach with a diversified portfolio reducing concentration risk

Horizon

One should look at investing for a minimum of 5 years or more

A systematic investment Plan (SIP) is an ideal way to take exposure as it helps tackle market volatility

Conclusion

The fund is the oldest fund with a proven track record of 35 years and has delivered 15.56% CAGR consistently. Thus, suitable for even first-time equity investors who are looking to take a little higher risk

DisclaimerThis is not recommendation advice. All information in this blog is for educational purposes only.

UTI Flexicap Fund

UTI Asset Management Company (AMC)

UTI is one of the pioneers of the Indian Mutual Fund Industry. With over Rs 2.4 lakh crore, the AMC is one of the most trusted names in the mutual fund space. The AMF offers products across asset classes.

Let us talk about its flagship product – UTI Flexicap Fund.

About Fund

1. Investment Objective

The fund seeks to generate long-term capital appreciation by investing predominantly in equity and related securities of companies in a flexible manner across the market capitalization spectrum.

2. Investment Process

The Fund follows a bottom-up stock selection method with well-defined metrics of free cash flows, capital efficiency, and ability to compound earnings.

The fund has a well-diversified portfolio and avoids sector as well as stock concentration.

3. Portfolio Composition

The portfolio holds the major exposure in large-cap stocks at 77% and sectorally major exposure is to financial services that account for roughly one-fourth of the portfolio.

The top 5 sectors hold nearly 70% of the portfolio.

Note: Data as of 30th Sep 2022. Source: UTIMF

Top 5 holdings

Name Sector Weightage % Bajaj Finance Financial Services 6.06 ICICI Bank Financial Services 5.59 HDFC Bank Financial Services 4.26 Infosys Information Technology 4.09 Kotak Mahindra Bank Financial Services 3.92 Note: Data as of 30th Sep 2022. Source: UTIMF

Fund performance over 30 years

If you would have invested 10,000 at the inception of the fund, it would be now valued at Rs 3.64 lakhs whereas the benchmark (Nifty 500 TRI) would have fetched you Rs 2.91 Lakhs.

Note: Performance of the fund since launch; Inception Date – May 18, 1992 Source: utimf.com

The fund has given consistent returns and has outperformed the benchmark over the period of 30 years by generating a CAGR (Compounded Annual Growth Rate) of 12.56%.

Fund Manager

The fund is managed by Ajay Tyagi. Mr. Tyagi has over 20 years of experience and has been managing the fund since January 2016. Mr. Ajay Tyagi, CFA is a Senior Executive Vice President and Head – Equity at UTI AMC.

In addition to managing a few domestic mutual fund schemes, he is also an investment advisor to a few India-dedicated offshore funds.

He is a CFA Charter holder from The CFA Institute, USA, and also holds a Master’s degree in Finance from Delhi University.

Who should Invest?

Investors looking to

Build their core equity portfolio by investing in quality businesses across all sizes

Invest in a fund with a disciplined approach to portfolio construction.

Why invest?

The fund shall comprise high-quality businesses that have the ability to show strong growth for a long period of time

Quality companies perform across the market cycle.

Horizon

One should look at investing for a minimum of 5 years or more.

A systematic investment Plan (SIP) is an ideal way to take exposure as it helps tackle market volatility

Conclusion

The fund is the oldest fund with a proven track record of 30 years and has delivered 12.56% CAGR consistently.

Thus, suitable for even first-time equity investors who have a moderately high-risk appetite and can remain invested for a long period.

DisclaimerThis is not recommendation advice. All information in this blog is for educational purposes only

Benefits of Short-term Goals

Short-term goals are specific and measurable goals that are easy to accomplish. The benefits of short-term goals are that it helps to bridge the gap between the present and where you want to be in the immediate future.

What are short-term goals?

Short-term goals are doable plans that are comparatively easy to achieve. These are realistic by nature as people can easily focus on them and are time-bound so that desired targets can be achieved in a shorter duration.

Short-term goals are short-period goals that can last for a few months and a maximum of one-year duration but not more than that.

Individuals can set short-term goals both in their personal and professional life. Some examples are learning a new skill, keeping a diary, building an emergency fund, saving for your child’s upcoming school trips, or saving money to pay quarterly school bus fees.

Benefits of Short-term Goals

1. Provides clarity to the overall plan

The short-term goals give a clear understanding of what the ultimate objective is and how to reach it in the best possible manner. It provides clarity to the overall plan because there is a definite plan of action with shorter and more manageable steps.

Parents who are interested in creating an education corpus for their children should segregate the goal into small manageable steps.

For example, think about the immediate future and invest in small-term schemes like 6-month FDs or school fees goals on the EduFund app to save for annual school trips or quarterly school fees.

2. Gives direction and maintains focus

The benefits of setting up short-term goals are that it gives direction to your thoughts and helps to maintain focus. Once the goal is set, the path becomes clearer because you have a plan of action that simply needs to be followed.

3. Helps to prioritize

Daily, weekly and monthly planning helps people to prioritize things based on their importance and decide what, how, and when they need to accomplish the targets.

Prioritizing filters out the unimportant things that do not matter at present and are simply distracting you from the main goals.

4. Prevents a feeling of anxiety

Setting up short-term goals reduces the to-do list considerably and stops an individual from being overwhelmed with work.

When you know that things are manageable, it will automatically reduce stress, and the feeling of anxiety will also minimize. Such goals keep people on the set path so that they are not burdened by things.

When an individual invests in short-term schemes, they can easily meet an immediate or sudden financial requirement which is not possible if the amount is invested only in savings plans that are most suited for long-term financial requirements.

This will help to relieve any anxiety caused by sudden expenses.

5. Time management

Setting short-term goals are beneficial as it encourages time management, like investing to pay a credit card debt. Individuals already have a target and a plan to accomplish set goals within the time frame.

6. Achieve measurable progress

Short-term goals are measurable goals with a clear path and an end destination in sight, for example, investing to buy a laptop. It becomes easy to set deadlines, track work, see the gains made and achieve measurable progress daily.

7. Inspires to move forward

When a person has a proper plan in place, it helps to maintain focus and walk on the path diligently. You can look back and measure your growth and improvement from the onset to where you are currently standing.

When people see progress, it inspires them to move forward with more grit and determination.

8. Build momentum

When the goals are short-term, individuals tend to be full of energy as they want to take action immediately.

It is possible to see the daily progress being made and keep track of how close you are to accomplishing the desired goals.

The excitement and energy to move forward act as a motivational tool and builds momentum.

9. Overcome procrastination

Procrastination is a serious threat to goals. The best thing about short-term goals is that people do not have the time for procrastination.

The goals have a set deadline which does not allow a person to waste time as they have a path to follow where every step is already defined, like saving INR 3,000 every month for eight months to buy a laptop for higher studies.

10. Increases self-confidence

Short-term goals are clear and specific by nature that will result in measurable outcomes. Individuals are fully engaged in their tasks and are also motivated to achieve them at any cost.

Daily progress and goal achievement boost self-esteem and increase self-confidence of a person.

11. Increases the chance of long-term success

Short-term goals give quick results and keep the motivation level high. People generally divide their goals into short, mid, and long-term goals like investing in FDs, mutual funds, ETFs, etc.

The reason is that they do not want to lose focus or direction midway. The short-term goals serve as appropriate building blocks for greater dreams.

When you have achieved several such goals, then the chance of long-term success automatically increases.

Conclusion

The benefit of short-term goals is that it motivates individuals to persist in their efforts and move forward. The chance of success is much higher as people do not lose their direction or focus.

In simple terms, short-term goals promote progress and growth in both personal and professional lives.

Consult an expert advisor to get the right plan

TALK TO AN EXPERT

Benefits of long-term goals. How to accomplish long-term goals?

The benefits of long-term goals are that it helps individuals to realize their dreams over time. Sometimes you need to prioritize and work things out.

Setting long-term goals gives people the opportunity to achieve desired results eventually.

What are long term goals?

Long-term goals are the desires, visions, or ambitions that people know will take some time to achieve. These goals are generally accomplished in the future.

The timeline varies from a few years to several years as the long-term goals cannot be achieved in a day, month, or even one year.

Long-term goals can be professional or personal goals like a young man of 20 wanting to become a manager at the age of 30, marrying and settling down by the age of 35, taking a break and traveling for six months by the age of 40, setting up an education corpus for a child or planning the retirement fund.

Benefits of long term goals

1. Gives direction

Without long-term goals, individuals will only think about the present and not think about the future, which as everyone knows is quite unpredictable.

Suppose an individual is earning INR 40,000 per month and does not have any long-term goals. He will then spend most of his salary without worrying about future consequences.

What happens if he suddenly falls ill or he requires a lump sum amount in the future? Long-term goals give direction, help people to think ahead, and make provisions accordingly hence they are beneficial in both personal and professional life.

2. Key to changing your life

Long-term goals act as a key to changing your life. Every person has a vision for a bright future.

The benefit of long-term goals is that it works as the inspiration behind the goals that motivate and urge to make dreams a reality.

Once the goals are set people often are encouraged to reach the end of the road by any means. They are no longer afraid of the difficulties in their path instead are driven to reach their goals.

3. Motivational tools

A long-term goal is an important motivational tool that gives the individual a focus point.

When you have set a long-term goal then you have a target to achieve and it becomes easy to work for and towards it with complete dedication and determination.

4. Increases self-confidence

Long-term goals inspire a better future and help you to see what you want and what you can achieve in the long run.

Measurable and specific long-term goals encourage a positive mindset, help to avoid procrastination, and increase productivity.

All these factors at the end of the day boost the self-confidence of a person.

5. Gives purpose to everyday actions

Setting up goals is not an easy task nor is moving towards it with complete dedication but once you set up long-term goals they can persuade a person towards his end goal.

Long-term goals give purpose to everyday actions and urge an individual to move forward even if the daily activities seem boring.

6. Encourages organized behavior

Breaking your goals into medium, short and long-term goals encourages organized behavior. It shows that the individual is capable of handling complex processes and prioritizing his objectives.

Long-term goals look scary at the beginning but with time it has the power to transform your way of thinking.

Individuals who set up long-term goals are seen to be more organized in their behavior and actions than people without any goals in their lives.

7. Take advantage of the full potential

Setting goals requires proper planning and when a person tries to set long-term goals he has to utilize his full potential.

He will have to find out his actual objective and research the best available means to reach the desired goals.

8. Helps in self-improvement

One of the important benefits of long-term goals is that it helps in self-improvement. People who set up these goals have to maintain their focus if they want to achieve such goals.

Long-term goals shape the direction of the thinking process and encourage people to move toward it diligently. It keeps on reminding you that you have done the hard work and only a little work remains.

The scope for self-improvement is immense as you have to improve your habits and move towards the goal somehow or the other to achieve them at any cost.

9. Achieve success

Long-term goals give people the time to align the necessary resources with the objectives in an effective manner.

It keeps you accountable, ensures better handling, and ultimately increases the chances of success.

INVEST NOW

Conclusion

The benefits of long-term goals are that it gives individuals the time to get a grasp on things and achieve them at a steady pace.

There is no need to overwork yourself instead people have the time to set a comfortable pace that is also achievable.

Consult an expert advisor to get the right plan

TALK TO AN EXPERT

Mutual fund vs Girl child schemes

Which is the better investment option for a daughter - MFs or girl-child schemes?

Indian parents are often on the lookout for the right kind of investment schemes that will lessen the financial burden of education and marriage expenses of their girl child.

They want to safeguard their child’s future and hence try to create a financial corpus as security for the days to come.

Before entering into a discussion about MF vs Girl Child Schemes, let us know about each of them in brief.

What is Mutual Fund or MF?

Mutual Fund refers to investment vehicles that accumulate money from several investors for buying a portfolio of various securities.

The portfolio includes several options like real estate, bonds, stocks, or a combination of different investments.

Investing in mutual funds is considered beneficial in recent times because of the high returns on investment. The most common drawback of a mutual fund is the high fees of the investor but this can be mitigated by choosing the right investor.

You can take the help of the EduFund App to reduce excessive charges with the help of saving experts.

What are Girl Child Schemes?

Girl child schemes are investment plans that offer benefits to the girl child. These are divided into two categories: State Government Schemes and Central Government Schemes.

Some of the highly popular ones are Sukanya Samriddhi Yojana, West Bengal Kanyashree Prakalpa, and Dhanlalakshmi Scheme.

The girl-child investment plans help parents to accumulate money so that it can later meet the financial requirements of the girl child.

Mutual fund vs Girl child schemes

Both Mutual funds and Girl Child Schemes serve the same purpose and that is to act as investment vehicles.

Parents often take the help of either of these or both to create an appropriate portfolio that will be able to meet the desired needs of their girl child.

Let us make comparisons and also see the difference between the two based on certain parameters.

1. Interest rates

Both schemes offer higher interest rates that lead to more savings. Girl child schemes generally offer a return of 7% to 8.6% whereas mutual funds offer returns of 12% to 14% easily in the long run.

2. Saving on taxes

Gains on equity funds, LTCG, ELSS, and dividends received on mutual funds can be claimed as tax-exempt as mutual fund investments up to INR1.5 lakh per annum are under tax deduction.

All the girl child schemes are exempted from tax to benefit the girl child.

3. Low minimum investment

Both schemes have the option of low minimum investment. Some investors have waived the minimums and individuals can now invest as low as $1 or INR 100.

There is already a fixed minimum value for a girl child scheme be it INR 200 0r INR 500 or INR 1000 and investors have to start with that amount only.

The Edufund App gives its investors the option of starting mutual fund schemes or SIP at INR 100 only.

4. Terms and conditions

The terms and conditions of the girl child schemes are straightforward with no room for any assumption. Mutual fund schemes are subject to market change and should be read properly by investors.

5. Limitation of amount

The minimum and maximum amount of investment in girl child schemes are pre-decided and you cannot go above or below the said amount.

Mutual funds on the other hand give the option of deciding the minimum and maximum amount by yourself as per your ability.

6. Flexibility

Girl child schemes do not offer any flexibility whereas investors can choose from a broad spectrum of mutual funds schemes.

7. Premium

In several girl-child schemes, the premium is waived off in case the policyholder dies prematurely, whereas that is not the case with a mutual fund.

8. Safe and secure

Although mutual funds are considered safe investments with greater returns, in the long run, girl-child schemes are a better option for conservative investors who are more concerned with the safety of their investments than high returns.

9. Partial Withdrawals

Several girl child schemes allow investors to withdraw partially after a specific period but mutual funds schemes have a specific lock-in period and cannot be withdrawn partially.

Conclusion

In the discussion between MF vs Girl Child Schemes, both the schemes are meant to benefit the investor at the end of the day.

If the investor is ready to take a certain amount of risk with their investment then they can create a financial corpus of a good amount through mutual funds.

But, if they are looking for a safe investment vehicle then girl-child schemes are the best option.

Consult an expert advisor to get the right plan

TALK TO AN EXPERT

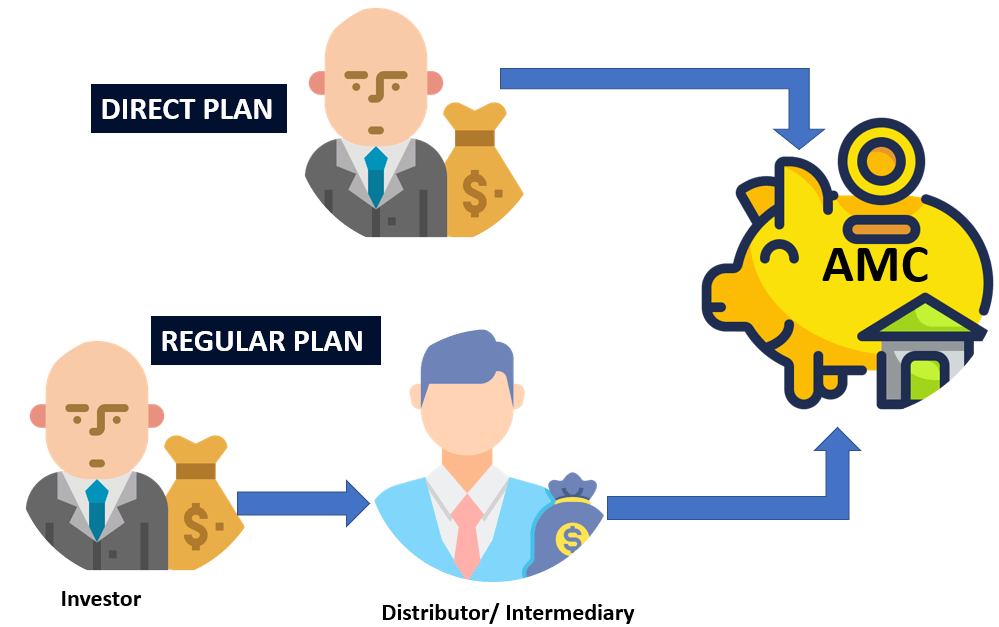

Direct Vs Regular Mutual Funds. Which is better?

Beginners are often torn between Direct vs. regular Mutual Funds. Every mutual fund is available to investors in two versions – Direct and Regular.

Regular plans involve an intermediary who manages the investments on behalf of the investor, whereas, in the direct plan, the investor directly deals with the AMC (as shown in the figure).

These versions are only the options available to the investor in the market that are offered by the same fund.

The invested amount from both options is managed by the same fund manager and has the same allocation of the assets in the fund’s portfolio

Only the road taken by the flow of money from an investor to the AMC is a different one.

Direct mutual funds vs Regular mutual funds

Here are the main differences between direct vs regular mutual funds

1. Direct Mutual Fund

Direct Plan is directly offered into the market by the AMC (Asset Management Company) or the fund house.

The investor can perform his/her own research based on their risk appetite, time horizon, and goals and then make a choice based on these parameters.

There is no distributor or intermediary involved, hence reducing the expense ratio (management fees charged by the fund house to the investors).

These plans can be easily identified as they are prefixed with the word “Direct” as a part of their name. The investors can choose an offline or an online mode to buy units of the fund.

Investors who can perform their research, and who also have the time and capability to manage their portfolio, prefer these plans.

2. Regular mutual fund

Regular Plans involve an intermediary and the investors invest through these distributors into the fund offered by the AMC. The intermediaries charge a commission or fee for their services to the fund house.

This fee is charged to the investor as a part of the expense ratio, hence the net fee when compared to direct mutual funds.

Due to the higher expense ratio, the returns tend to be lower than the direct plan counterparts. These plans provide convenience and are preferred by investors who have less knowledge about the markets.

Parameter of differenceDirect Mutual Fund PlanRegular Mutual Fund Plan Expense RatioLowerHigherNAVHigher than RegularLowerReturnsHigherLowerIntermediaryAbsentPresentFinancial/Investment AdviceNoneAvailable and provided by the advisorResearch on where to investSelf – To be done by the investorProvided by advisor

Why are Direct plans better?

1. Lower expense ratio

Did you know that you pay for the financial advice that the distributor gives you? The intermediaries charge it to the fund house as a commission.

However, this commission paid to the advisor is charged as a part of the expense ratio to the investor. Hence, the investor indirectly pays the intermediary.

The fee which is deducted for the advisor varies from 0.5% to 1%. In the case of a direct mutual fund, there is no intermediary, hence there are no distribution charges or commissions to be paid, resulting in a lower expense ratio.

Over a longer horizon, the small % of fees paid out of your pocket makes a large difference to the final corpus that is accumulated.

Consider the Axis Bluechip fund which has earned the following returns over the last 5 years and has beaten its benchmark (Nifty 50 TRI).

Consider two scenarios where the investor invests Rs 10 lakh into this fund through a Direct plan in one case and in a regular plan in the other.

However, the small difference of 1.44% leads to a large change of Rs 1.36 lakhs to the final wealth that is accumulated. (Data of returns are from AMFI website)

ParametersDirectRegularDifference5-year returns18%16.56%1.44%Initial Invested Amount10,00,00010,00,0000Final Corpus accumulated 22,87,758 21,51,531 1,36,226

2. Higher Returns

The returns from a direct plan are always higher than the returns from the regular plan, owing to the higher expense ratio. Returns being one of the most important factors for cherry-picking the fund of your choice, this difference should be taken into consideration.

Some of the examples of the funds are as follows: (Data of returns are from AMFI website)

5-year returnsDirectRegularAxis Bluechip Fund18%16.56%Aditya Birla Sun Life Mid Cap Fund 12.56%11.53%Axis Small Cap Fund19.70%18.17%

3. Higher NAV

Net Asset Value or NAV = Assets of the fund - Liabilities of the fund / Number of units of the fund

The assets owned by the fund include equity or stocks invested by the fund, debt instruments such as debentures or government securities, and cash.

The liabilities of the fund include money owed to banks, fees to distributors or other associated entities, etc.

In the case of the direct plan, due to the absence of the fees, the Net Assets (Assets – Liabilities) are higher resulting in a higher NAV.

Whereas in the regular plan, the fees/commission to the distributor or intermediary forms a part of the liabilities, reducing the NAV. A higher NAV would imply a higher investment value.

Differences between Direct and Regular Plans

The key difference between direct and regular mutual funds:

Net Asset Value (NAV): The key difference between direct and regular mutual funds is NAV. The NAV of a direct plan is higher than the regular plans. This means that the value of your investment is more in a direct plan than in a regular plan.

Returns: Returns are likely to be higher in direct plans over regular plans. This is because regular plans charge a fee for the advisory role and that can affect your overall investment value.

Role of financial advisor: Direct plans do not offer financial advisory services or expertise. You are required to research by yourself, determine the best fund, and time the market to understand the best time of investment and exit.

All these decisions and market research is taken care of by professionals with regular funds. These are regularly monitored and adjusted to help fetch the best returns in the market.

Direct Plan – Mutual Fund Regular Plan – Mutual Fund Higher Returns Low Returns Low expense ratio High expense ratio NAV- High NAV - Low Self-Researched & Monitored Researched & Monitored by Advisor Advice is not provided Advisory services provided by experts SIP/Lumpsum available SIP/Lumpsum available

FAQs

Which is better direct or regular mutual fund?

Direct mutual funds offer higher returns in the long run to investors. However, investing in mutual funds requires market research and financial expertise which is offered by a regular plan.

Both are good investments and benefits are likely to vary based on the investor and their choices.

What is the difference between direct and regular mutual funds?

In regular mutual funds, AMCs are required to pay a commission to the brokerage. This is not the case under a direct mutual fund. Direct funds have lesser costs involved, a higher NAV, and are do-it-yourself funds where the investor must make investment decisions on their own.

Why Invest in a Regular Plan of a Mutual Fund?

The biggest benefit of a regular plan in mutual funds is the financial advice offered by the Fund house. This can have a huge impact on your returns and you can get closer to your financial goals more efficiently.

Conclusion

In conclusion, apart from the above benefits, one is always in control of their investments and is also well informed about the turbulences in their portfolios and aids in taking an active approach towards the financial goals.

A tiny % of difference can multiply into a larger difference in the final returns from your portfolio. One can learn about the AMC, the mutual fund options available that suit your risk profile from the services offered by wealth management sites such as EduFund, with a minimal fee, when compared to the expense ratios of a regular plan.

The next time that you plan on investing in a mutual fund, go for a direct plan. It will surely involve some initial research and some preliminary work, but you will be able to reap long-term benefits from making this wise choice.

Top 5 Best Film Schools in the World

Getting into one of the best film schools in the world is no joke. But once you get through, you can expect future rewards of fame and recognition in the movie industry.

Choosing the best school for you is a task that you cannot afford to take lightly because you have to consider not only the school's international ranking but also its faculty, departments, courses, and the practical equipment available.

Another critical factor is the tuition fee and the cost of living, particularly in the case of global education. Choose a school that will set you up for a career with great returns because film studies courses are anything but cheap. Here is a list.

Best Film Schools in the World

1. USC School of Cinematic Arts, USA

Located in Los Angeles, USC or the University of South California School of Cinematic Arts is unanimously considered the best in the country, funded by the likes of George Lucas.

With its million-dollar funds, it can afford to provide students and research scholars with luxury amenities like an IMAX theatre and labs. USC School of Cinematic Arts is also one of the oldest. It was founded in 1929 along with the Academy of Motion Picture Arts and Sciences.

The School has many divisions including Cinema & Media Studies, Film & Television Production, John Wells Division of Writing for Screen & Television, John C. Hench Division of Animation and Digital Arts, Interactive Media & Games, Media Arts and Practice, and Peter Stark Producing Program.

It offers a range of courses in film studies including BA, BFA, and MFA. Various renowned film directors, cinematographers, animators, producers, researchers, and so on, form the alumni of this film school.

2. National Film and Television School, UK

National Film and Television School, popularly known as NFTS, has been ranked as UK’s best for many years. Despite being located on the outskirts of Northwestern London, NFTS is quite famous amongst film scholars.

It was established in 1971 and stands out amongst the film schools in the UK because of its amazing curriculum.

The well-known American e-mag The Hollywood Reporter has listed NFTS among the best international film schools in the world in 2021.

Among the alumni of NFTS is David Yates, the director of the Harry Potter movies. Other than offering a good number of specialized PG courses, it also offers diploma and certificate courses.

3. American Film Institute, USA

American Film Institute is undoubtedly the best one in all of LA and definitely one of the top 5 film schools in the world. If you are aspiring to attend the coolest film school in the world, AFI is the answer to your prayers.

It offers you the opportunity to produce your own short projects during your course. If these works are extraordinarily good, you also get the opportunity to meet legends like Steve McQueen for personal training in the art of filmmaking.

AFI was established as a film organization in 1965 to train budding American filmmakers in motion picture arts and runs on private funding.

David Lynch, who is known for his critically acclaimed works, also has a special inclination toward this film school.

4. Beijing Film Academy, China

Beijing Film Academy or BFA is the most sought-after film school in all of Asia. BFA started a small institution called the Performance Art Institution of the Film Bureau of the Ministry of Culture in 1950.

But by 1956, the name was changed to Beijing Film Academy. Currently, it is one of the largest film schools in the world.

Film Industries are witnessing exponential growth in Asia and this makes BFA a great choice. Also, personalities like James Cameron have been part of it as visiting fellows.

The curriculum is vast with Bachelor’s, Master and associate courses in various areas like film theory, directing, producing, acting, animation art, cinematography, sound art, and scriptwriting among others.

5. La Fémis, France

La Fémis connects one to the rich history of filmmaking which began with the Lumiere brothers in 1894. This French institution is based in Paris on the very site of the Pathé studios which is where filmmaking itself originated.

La Fémis has produced famous filmmakers in the past who have made history at the Cannes Film Festival, Berlin International Film Festival as well and Venice Film Festival.

It even precedes the Tisch School of the Arts of New York City and China’s BFA in being one of the most rewarded schools worldwide. The main curriculum is a self-designed 4-year course based on a fine balance of theory and praxis.

Best Film Schools in India

Film and Television Institute of India, Pune

Satyajit Ray Film and Television Institute, Kolkata

National Institute of Design, Ahmedabad

Whistling Woods International, Mumbai

Ramesh Sippy Academy of Cinema and Entertainment, Mumbai

Asian Academy of Film and Television

LV Prasad Film and TV Academy, Chennai

Centre for Research in Art of Film and Television (CRAFT), Delhi

The ICE Institute

KR Narayanan National Institute of Visual Science and Arts

Kalapurnam Institute of Visual Effects and Animation

Best Film Schools in Europe

London Film School

National Film and Television School

Academy of Performing Arts’ Film and TV School

La Femis

Lodz Film School

London Metropolitan University Sir’s John CASS Faculty of Art, Architecture and Design

University of Television and Film Munich

National Film School, Italy

National Film School of Denmark

Norwegian Film School

Screen Academy Scotland

University of the Arts London’s College of Communication

Russian State University of Cinematography

FAQs

Which is the best film school in the world?

The Los Angeles Film School, California

Toronto Film School

Vancouver Film School

London Film School

Academy of Performing Arts Film and TV School

La Femis

Lodz Film School

Beijing Film Academy

Which is the hardest film school to get into?

One of the hardest film schools to get into is the University of Southern California’s School of Cinematic Arts. Only 3% of applicants are admitted to the School of Cinematic Arts.

Which college has the best film school?

American Film Institute

California Institute of the Arts

Chapman University

Columbia University

Emerson College

Loyola Marymount University

New York University

University of California, Los Angeles

Which country has the best film schools in the world?

The United Kingdom tops the list as it has some of the best film schools in the world. Reputed universities and award-winning alumni from the best universities in the UK make it a most sought-after destination for film studies.

Conclusion

Preparing to get admission to one of the best film schools in the world can feel like a full-time job in itself. Knowing the basics about these schools is a good start to that journey.

Once you are aware of what you are signing up for, you can attain more determination and tenacity for realizing your dreams.

Consult an expert advisor to get the right plan

TALK TO AN EXPERT

Is there the best date of month for SIP investment

Mutual fund companies offer flexibility to invest in their schemes through SIP (Systematic Investment Plan).

While some choose the date of SIP based on their salary credit, others may try to time the market by selecting specific dates based on different factors one may choose to invest at the end of the end because of the high volatility and F&O expiry of the month-end contract.

So, is there a best date for SIP investment?

In this blog, we’ll see whether the date of SIP will make a huge difference or not.

Read on!! We have analyzed the data of the past ten years, from Jan’11 to Sep’22, of BSE Sensex based on daily returns to understand it in a better way.

Note: When there is a holiday, the date of the previous/next working day has been considered.Source: BSE, EduFund Research Team

The above calculation shows that there is hardly a marginal difference in returns based on the period under observation. So, there is no strong relationship between the SIP date you choose and the returns.

Any date will work if you are investing through SIP. Experts suggest that one should never try to time the market; instead, remain invested with discipline over a longer period to get the most benefit of compounding.

SIPs are designed to deal with the volatility in the market. SIP helps your investments to average out the cost of buying, which is called rupee cost averaging.

This helps investors to buy mutual fund units at lower prices and higher, which averages out the cost of buying the units.

What is Compounding?

Compounding works as a multiplier in your investment. You not only get the returns on the invested amount but also get the returns that keep getting added back to your invested amount.

In short, earning returns on principal & returns as well. The best thing about compounding is that at one point your amount of returns will be more than your invested amount.

What is the rupee-averaging cost?

In this concept, a fixed amount is invested at regular intervals. This allows you to buy more units of a mutual fund when prices are low and fewer units when prices are high. Over the period, this averages out the cost of buying.

Timing the market is challenging. The market goes through different phases, and you never know when the market is going to rise or fall. So, disciplined investing will help you to accumulate wealth over the period.

When we try to time the market, we invest with emotions which can lead to wrong decisions. SIP helps to ignore all these factors and helps to invest regularly.

Conclusion

SIP can do wonders with your investments if you do discipline and regular investing over a longer period without thinking of the date, by Just following the normal process.

Consult an expert advisor to get the right plan

TALK TO AN EXPERT

What’s in store for you this Samvat 2079?

The Indian markets recovered and boomed in November 2021, followed by a sharp decline of 9-10% from January 2022 until June 2022.

The fall continued, with the single most significant fall of 2.5% in September 2022. Investors have been cautious about what the D-street will offer them during Samvat 2079 Muhurat.

Let us see how the market has performed for every Samvat

Samvat se Samvat Tak - Nifty performance Note: According to the Hindu Calendar, the Vikram Samvat calendar is 56.7 years ahead of the solar Gregorian calendar. Hence, when the Gregorian is in 2022, it is the beginning of Vikram Samvat 2079, which will be post-Diwali next week Source: Economic Times, EduFund Research

For global equities, Samvat 2078 turned out to be a challenging year, given headwinds including rate hikes, the energy crisis, the Russia-Ukraine conflict, continued supply disruptions, outflows from foreign investors, and heightened inflation.

What does the index indicate this Diwali?

India’s equity market is likely to outperform its global peers in the upcoming Hindu year of Samvat 2079. This will be on the back of improving corporate earnings.

Cumulative profits of the top 500 companies as a percentage of the country’s gross domestic product (GDP) hit an 11-year high of 4.3 percent in 2021-22 (FY22).

This has been a positive sign of revival after the massive destruction caused by COVID-19.

Corporate earnings to GDP ratio – an all-time high for India with a sharp rebound post-COVID.Note: According to the Hindu Calendar, the Vikram Samvat calendar is 56.7 years ahead of the solar Gregorian calendar. Thus, when we are in 2022, it is the beginning of Samvat 2079 which is after Diwali next week. Source: Economic Times, EduFund Research

Going by the GST and advance tax collections, for the second quarter of FY 2023, the aggregate revenue for the Nifty 50 companies is likely to witness a healthy double-digit growth of up to 20% year-on-year.

This will be a massive improvement for the seventh quarter in a row and will be led by strong credit offtake. A revival in private capital expenditure due to stocking up of goods before the festive season.

Amid inflation concerns and higher input costs in India, some of the factors which have worked well for the Indian economy are healthy GST collections, the highest GDP growth in the Asian region, an above-normal monsoon, and strong earnings.

These factors are likely to keep the economy in better shape when compared to other emerging economies, particularly at a time when there is a lot of uncertainty around the global market.

On the FII and DII movement, the market has seen a heavy withdrawal in 2022 particularly in Q1 and Q2 of CY 2022 due to non-competitive interest rates, geo-political issues, inability to beat inflation, and better return opportunities in other markets.

However, the FIIs generally love pouring money during Muhurat trading due to its favorable market conditions and there have been signs of declining FII withdrawal from the Indian market in Q3. This is likely to provide the much-needed impetus to the Indian market.

How has the FII/DII participated in the market?

Note: Net Purchase / Sales of FII/DII in Cash Source: Moneycontrol

How are the valuations?

With the recent correction in the market, and the improving earnings of India Inc. the valuation as defined by the P/E ratio has fallen in line with the long-term average for CY22.

This makes the market more attractive from a long-term investor point of view.

Note: Simple Average is taken for the yearly P/E ratio Source: Nifty PE Ratio, EduFund Research

Particularly for 2022 after April, the valuations have been becoming attractive owing to improving earnings and also correction in the market.

Note: Data for Nov and Dec 2022 is not available Source: Nifty PE Ratio, EduFund Research

What should you do?

The Indian markets have faced a significant hit and have performed the worst in September 2022 due to rising inflation and interest rate hikes.

However, we believe any correction in the market is inevitable and should be used as an opportunity to acquire more units of investment to make the most of the opportunity.

The Indian benchmarks are currently trading at rich levels, and we have an optimistic view with regard to the Indian economy’s growth.

This is primarily due to the reforms the government and the Central Bank are taking to beat the rising inflation and improve private capex.

Additionally, we are bullish that several multinational companies have been moving their units from China to India, with Apple starting its facility in India.

Having said this, one cannot ignore the harsh reality of high inflation, declining currency value, and rising geopolitical issues with tensions between the US and North Korea and Russia and Ukraine.

Also, with a high probability of another rate hike by the US Fed later this year and the depreciating rupee, Indian inflation is likely to stay high next year.

Thus, it would help if you focused on single names that perform well in a volatile environment and are undervalued, as highly valued stocks are less likely to perform during periods of inflation and high-interest rates.

For investors who are less adaptable to a volatile environment, mutual funds work the best, particularly in the hybrid category with a dynamic asset allocation approach.

DisclaimerThe Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in this content constitutes a solicitation, recommendation, or endorsement. Please consult your advisor before investing. Mutual Funds are subject to risk, read the offer documents carefully before investing.

Difference between Equity vs Debt funds. Which is better?

Equity vs Debt Funds which one is better is an ongoing discussion between investors who are interested in mutual funds as their investment vehicles.

Although both these funds are good investment schemes each of them behaves differently when it comes to various parameters like returns, taxation, duration, and investments.

The selection of a specific fund depends upon personal preference, risk appetite, and the financial goal of the investor.

Some investors find it difficult to distinguish between equity funds and debt funds. Let us get a better understanding of both investment options so that the knowledge can help to make viable decisions.

What is an Equity Fund?

Equity funds are mutual fund schemes with investments in company shares and related securities like derivatives (futures and options) that trade in the stock market and have the potential to grow rapidly.

The objective is capital appreciation and dividend-paying stocks that provide an income to the investor.

Equity funds are categorized as large-cap, small-cap, mid-cap, and thematic funds. When a fund manager invests more than 65% of the portfolio in stocks it is considered an equity fund.

What is a Debt Fund?

Debt funds are mutual fund schemes with investments in securities and money market instruments that generate fixed income.

These are corporate bonds, commercial papers, treasury bills, non-convertible debentures, certificates of deposit, and government securities.

Debt funds are secure investments, with lower returns and a fixed maturity period.

Differences between Equity vs. Debt Fund

1. Instruments

Equity funds invest in company shares traded in the stock market and securities and derivatives like options and futures whereas debt funds invest in debt and money market instruments like corporate bonds, commercial papers, treasury bills, non-convertible debentures, certificates of deposit, and government securities.

2. Return on investment

Equity funds yield higher returns in the long run whereas the return on investment in the case of debt funds is low to moderate when compared with equity funds.

3. Tax saving options

Investors can save taxes by investing in ELSS mutual funds up to INR 150,000 per year. There is no such tax-saving option for investors in debt funds.

4. Risk appetite

Investors with moderately high to high-risk appetites opt for equity funds whereas investors with low to moderate-risk appetites choose debt funds as their investment vehicle.

5. Timings

The timings of both buying and selling of equity funds are very important as they are dependent upon the stock market which is known for its volatility.

The timings of buying and selling in the debt funds are not as important as it is for equity funds. The duration on the other hand is more important than the timing for a debt fund.

6. Expense Ratio

In equity vs debt funds, the expense ratio of equity funds is much higher as it is managed by fund managers whereas the expense ratio of debt funds is lower when compared with equity funds.

7. Taxation

Investors have to pay a 15% tax on capital gains from equity funds that are held for less than 12 months. The capital gains on equity holdings for more than 12 months are tax-exempt up to an amount of INR 1 lakh.

All the gains beyond this amount are taxed @ 10%.

In equity vs debt funds, if investors are holding debt funds for less than 36 months then they will have to pay short-term capital gains tax and it will be taxed as per the tax bracket of the investor.

When the debt holding is for more than 36 months investors can avail of indexation benefits and post it the long-term capital gains are taxed at 20%.

8. Investment duration

Equity funds are investment options for the long run as they help investors to meet long-term financial goals.

Debt funds are investment options for the short run as the duration ranges from 1 day to several years. These are often used as alternatives for savings and fixed-deposit bank accounts.

How can one invest in equity or debt funds?

Investors can take the help of financial advisors at the Edufund App for informed decisions as the platform offers an option to choose from 4000+ mutual funds in both equity and debt fund categories.

The platform guarantees transparency and secured transactions because of top-class 128-SSL security.

Moreover, the value-added benefits like zero commission, no hidden charges, free advisory, and tracking investments through Edufund’s scientific fund tracker help to save a good amount that can be invested further in either or both equity and debt funds.

Conclusion

In the discussion between equity vs debt funds, it is important to note that these are tax-efficient investments when compared with other asset classes.

Both are mutual funds that help investors to meet their investment goals effectively.

FAQ

Which is better debt fund or equity fund?

Equity funds generate slight higher results

Which is riskier debt or equity?

Debt has a real cost to it, the interest payable

Is SIP in debt fund good?

All debt funds are not suitable for SIPs

Are debt funds good for the long term?

Investors should invest in long-term debt funds if they have an investment time frame of more than 3 years

TALK TO AN EXPERT

Low expense ratio mutual funds in India

When choosing a mutual fund, you need to consider factors like risk, performance, fund portfolio, and expense ratio.

The Total Expense Ratio, or TER, is one of the most important factors to know about before investing in a mutual fund.

Let's see why you need to study it, what are expense ratios, and the best mutual funds with low expense ratios for you to consider.

What is the Expense ratio?

Mutual Funds incur certain operating and expenses for managing funds like – sales & advertising expenses, transaction costs, investment management fees, registrar fees, etc.

The expense ratio includes all such expenses incurred by the Mutual funds. It is adjusted to the fund's Net Asset Value (NAV). It is adjusted daily and is a cost to the investor.

How does the Expense ratio make a difference?

Let's consider the actual difference expense ratios can have in the wealth created.

Here, we have taken two types of PGIM India Midcap Opportunities Fund – regular and direct. The time period taken is ten years.

Scheme SIP Annualized Returns Expense ratio Final corpus (Rs.) Direct 10,000 21.01% 0.40% 1,26,35,714 Regular 10,000 18.96% 1.95% 1,01,62,185

By investing in a regular fund, you incur an expense ratio of 1.95% compared to 0.40% in the direct mode. This expense ratio has cost the investor an additional Rs. 24,73,529.

This means that by investing in a regular fund, you lose almost 24 lakh rupees! The gap increases significantly when this is compounded for larger SIP values and for longer time horizons.

With lower expense ratios, the wealth creation in a portfolio increases to a great extent.

Mutual Funds with a low expense ratio

Scheme name Category Expense Ratio Returns (3yrs) Mirae Asset Tax Saver Fund ELSS 0.50% 19.91% PGIM India Mid Cap Opportunities Fund Mid Cap 0.40% 38.48% UTI Nifty 50 Index Fund Index 0.20% 14.57% Canara Robeco Small Cap Fund Small Cap 0.39% 39.01% HDFC Index Nifty 50 Fund Index 0.40% 13.80% *Disclaimer – This is not a direct recommendation

How to reduce the Expense ratio of your funds?

Choose a fund with a low expense ratio in respective asset classes. But at the same time, remember not to compromise on the return aspect of the fund because if the fund has low-risk adjusted returns, then having a low expense ratio will not benefit your portfolio.

Adopting a passive approach to investing significantly reduces the expense ratio. For example, instead of investing in a blue chip or a large-cap mutual fund, you can choose a Nifty 50 Index Fund, which comprises the same large-cap companies' stock but has a lower expense ratio than the former.

Last but not least, always choose Direct Funds instead of Regular ones. This way, you don't have to pay an additional commission to distributors.

Should expense ratio be a deciding factor when choosing your mutual funds?

Definitely not! The major factors you should consider while choosing a mutual fund are the risk-adjusted returns, the performance, the portfolio composition, the standard deviation, the fund managers' performance and experience, and whether or not it fits your investment objective.

The expense ratio should only be one of the above factors to compare two or more mutual funds in the same category offering similar returns but not a deciding factor.

For instance, funds may generate better returns than the category average but with a slightly higher expense ratio. You may consider the power of compounding with the returns generated in such cases.

Conclusion

Never choose a fund solely based on the expense ratio. Always perform a detailed fundamental analysis to ensure you choose the right fund for you and your portfolio.

This will make your investment journey smooth. If you find it challenging to choose a mutual fund that's right for you, take the help of an investment advisor who will guide you through the entire process.

Consult an expert advisor to get the right plan

TALK TO AN EXPERT

Key milestones to plan for child investment plans

To guarantee a bright financial future for your kids, you must have a solid financial strategy.

It's crucial to base your investments on the aspirations of your children and anticipated cash flow needs. In this blog, we have discussed the key milestones to plan for your child's investment plans.

School

When budgeting and preparing their investment for their child's education, parents should expect the primary school tuition price, and expenses like uniforms, books, extracurricular activities, transport fees, yearly vacations, picnics, etc., to be between (INR 1.25 - 2 lakh per year).

Higher Education

While planning for your child's higher education The yearly cost of study and living is the first and most important element that one has to take into account before enrolling in college.

Universities offer housing on their campuses for both domestic and international students. However, if the institution you have selected to attend does not provide this amenity, you may simply obtain personal accommodations.

Following are the estimated costs of studying UG and PG courses from India and abroad:

Govt Colleges in India will cost around Rs 5-6 lakhs.

Private Colleges in India will cost around Rs 8-10 lakhs.

Studying Abroad can cost up to INR 1 crore.

Marriage

Although it is stated that marriages are created in paradise, they take place on Earth and require a lot of money to make them memorable. You arrange your "Big Day" to be a special occasion for both you and the family that attend the ceremony.

The Indian wedding market is presently worth over Rs. 1,000 crores and is expanding quickly, at a pace of 25–30% annually. The average cost of a wedding in India ranges from INR 20 lakhs to 5 crores.

According to estimates, the average Indian spends one-fifth of his lifetime earnings on his wedding. Also, you need to assemble a skilled team, including event planners, florists, caterers, and fashion designers, to make your special day extraordinary.

Therefore, before investing in a child investment plan, you must make plans for each of these milestones for your children. Below, we have included the investment strategy and several investment options for your kid's future.

Investment strategy for children's investment plan

List specific goals upfront, such as the child's preferred education and related costs. After paying all of your regular costs, you'll be able to estimate how much you can afford and how much you'll need to set aside each month.

However, you must remember that loans can also be utilized to fund your education. As a result, you do not have to sacrifice other expenditures like healthcare and retirement to save for your child's education.

As the financial goal approaches, reduce your stock exposure to lessen the likelihood of adverse market changes.

Different investment options for your child

Fixed deposits and other traditional products might not be enough to cover your child's college costs. Other products like equities funds, balanced funds, and shares should be taken into account.

You can select one of the following investment strategies depending on your time frame:

The best option is debt mutual funds if your child will need the money within five years. Such funds can provide liquidity while producing returns that are more than the rate of inflation.

You can mix several financial products for long-term aims. You have the option of investing in gold, stocks, and debt. Although exposure to the stock market is hazardous, investing in equities allows investors to generate larger profits over the long run.

PPF is one of the greatest investment options for financing a child's education. To establish a sizable corpus, you must begin this early and invest steadily.

Numerous insurance providers provide a range of kid-focused solutions. When your child needs the money to pursue further education, you may choose to implement more mature policies.

FAQ

Which investment is good for a child's future?

When your child is still small and you have at least 15 to 20 years till retirement, it is excellent to begin investing in equities mutual funds.

This enables you to withstand shocks like stock market collapses and volatility.

Why is future planning important for children?

The best way to guarantee money for your children's future needs is through child plans. Many modern plans come with a variety of features that can help you develop your assets and ensure that your kids have money for college.

Without having to deal with the pressure of a large investment, you may frequently make little investments.

When is the best time to buy a child's education plan?

Generally speaking, it is best to get a kid's education plan as soon as possible. This is so that you can leverage the benefits of compounding if your investment has more time to develop.

Investment plans for children help you and your child prepare financially for growing education costs, unanticipated illnesses, and bad circumstances. Planning for your child's future must begin as soon as feasible. This spreads out the risks involved and gives your assets more time to flourish

TALK TO AN EXPERT